Here’s the move I’m making—and you can too, if you’ve got $7500 in available cash sitting around. It’s a straightforward, cash-secured put strategy designed to bring in $350+ after commissions.

Selling to Open: 6 March 20, 2026 $12.50 Put Options [Symbol: LEG260320P12.5]

Limit Order Price: Credit of $0.60 per share

Rationale for the Trade

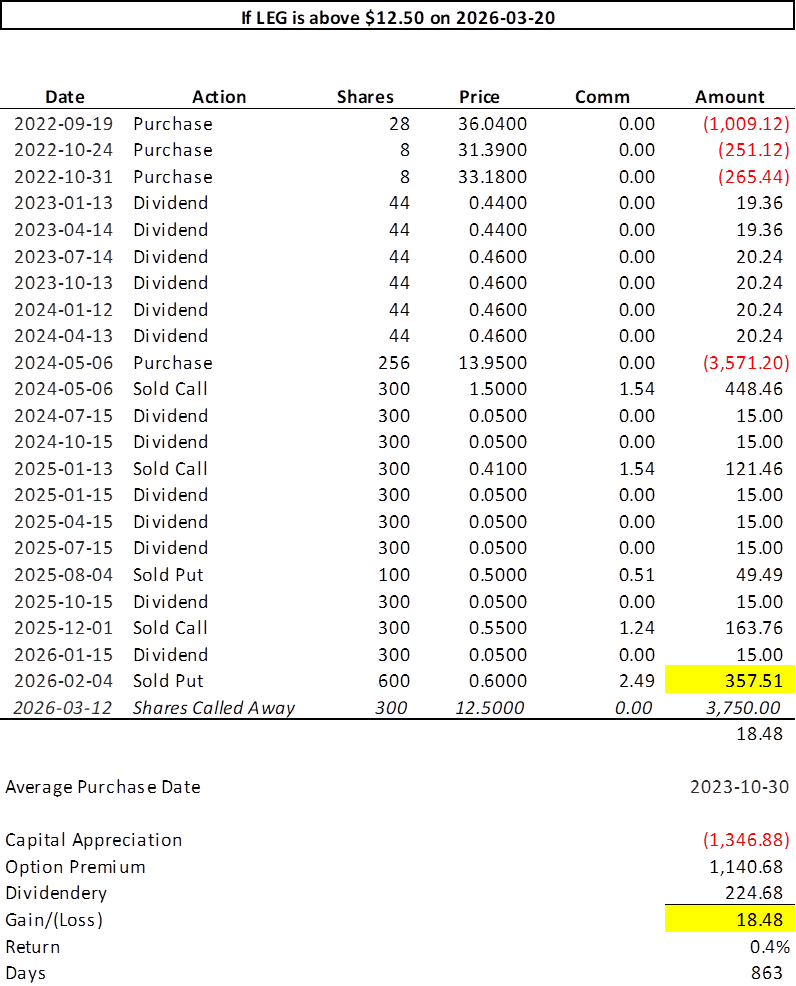

On March 20, 2026, LEG will either finish above $12.50 or it won’t. After selling these six puts, we can evaluate how the position behaves under each outcome.

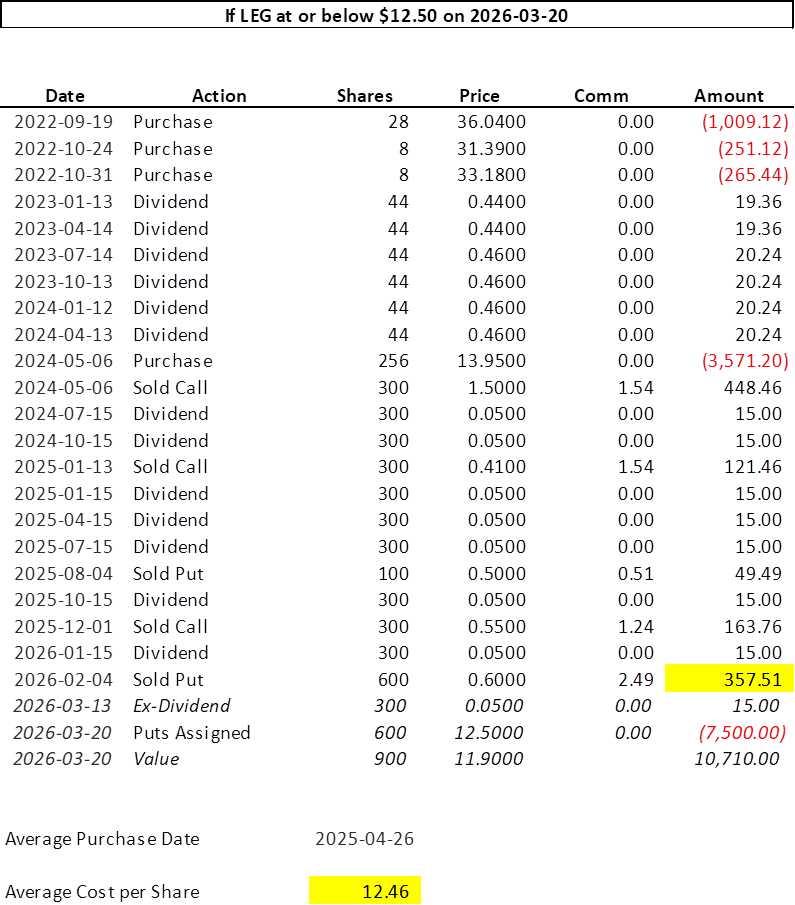

First, I am choosing to introduce a little conservatism here in assuming that shares would actually be assigned prior to the ex-dividend date of 2026-03-13. If LEG is trading above $12.50 a week before the expiry, the shares would very likely be called away on the 12th so that the individual receiving those shares would be the holder of record in time to receive that next dividend. Leaving it out above understates the total profit by $15.00.

Second, and most importantly, the $357.51 received with the sale of the puts is just enough to put this position in the black. With LEG above $12.50 those puts expire worthless and the three calls we sold means the 300 shares we own are called away.

And that would be all she wrote for LEG as a position in the Portfolio for the Ages until they string together another 50 consecutive years of dividend increases.

Worst‑case scenario: LEG drops back below $12.50 and we’re assigned on all six puts, committing $7,500 to a position we’d prefer not to expand. That may sound dramatic, but it’s a calculated risk built into the trade.

In this outcome, we still collect the full $15.00 in premium. More importantly, once those 600 shares are added, the average cost per share—after accounting for all dividends and option premium collected—falls to $12.46. That’s just under the ever‑present $12.50 strike that appears in every monthly option chain.

With that new basis, the next step is straightforward: turn around and sell nine covered calls expiring in June. That generates a strong premium and gives us a high probability of eventually getting called away at a profit—and at a better profit than in the first scenario.

To illustrate the scale of the position, assume LEG is trading at $11.90 on 2026‑03‑20. That happens to be the breakeven price for the puts sold at $0.60 each.

Could the shares be significantly lower on that date, creating a deeper hole to climb out of? Yes.

Is that the likely path? I don’t think so. Two points matter here:

- The stock has held above $10.75 for more than two months.

- On 2026‑01‑20, LEG issued a press release announcing that it had entered into a non‑disclosure agreement with Somnigroup. In that same release, the Board stated unequivocally that “Somnigroup’s $12 per share proposal undervalues the Company,” and formally declined the offer. At the same time, by opening their books and allowing Somnigroup to begin due diligence, the Board made it clear they would consider a sale — but only if a more appropriate and higher offer is proffered. The $12.00 offer should now act as the de facto floor.

Could the shares blast off with a great earnings report on 2026-02-11? Yes. There is nothing we can do about that though. The calls were sold at $12.50 to allow for some breathing room above that $12.00 purchase offer. The next highest strike price was (and still is) $15.00 and because that offer was made for $12.00, the $15.00 had almost no premium associated with it. And that is still the case.

LEG sells mattress springs for crying out loud. If they blast off a week from now, so be it.