We’re facing what I believe is a rare and compelling opportunity: a broad, tariff-driven market sell-off has created mispriced assets across the board. LEG took a sharp hit following its Q2 2025 earnings release—not, in my view, due to company-specific weakness, but as collateral damage from the wider market reaction.

Here’s the move I’m making—and you can too, if you’ve got $750 in available cash. It’s a straightforward, cash-secured put strategy designed to capitalize on temporary dislocation while positioning for long-term value.

Selling to Open: 1 October 17, 2025 $7.50 Put Option [Symbol: LEG251017P7.5]

Limit Order Price: Credit of $0.50 per share

Rational for the Trade

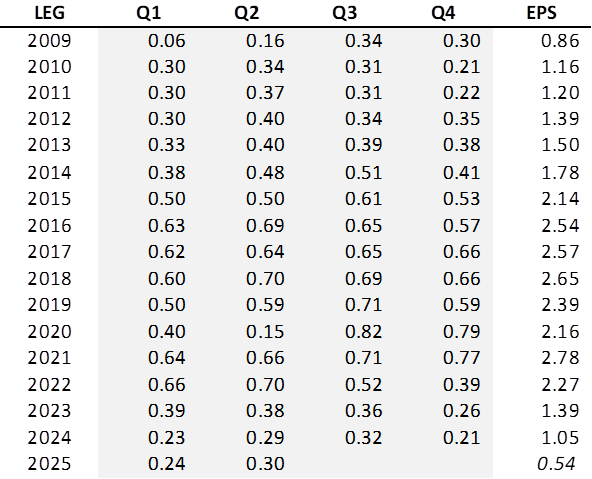

2025Q2 EPS [Adjusted, Diluted Non-GAAP] of $0.30 beat analyst estimates by less than a penny, exceeded last quarter and exceeded 2024Q2 on 6% lower revenue. Their guidance for the year remains unchanged from $1.00 to $1.20 EPS.

But more importantly, management believes tariffs will be a net positive going forward. Of course, they acknowledge that tariffs, and their related announcements are more liquid than water, but the profit margins related to steel in particular outweigh some of the other, more negative effects. Further, there is acknowledgement that tariff-induced consumer behavior could easily swing the effect of tariffs into a net negative.

More concretely, and for me the most important aspect of their latest quarterly report was that LEG strengthened their balance sheet with total debt reduction of $143 million during the quarter. This has led to an improved net debt to 12-month trailing adjusted EBITDA ratio of 3.51. In fact, the debt-to-equity ratio over the last six quarters has played out thusly: 3.61, 3.83, 3.78, 3.76, 3.77, & 3.51. The 3.5X is a massive improvement and it satisfies the covenant of their (now favorably amended) revolving credit facility.

LEG is by no means out of the woods, but they’re delivering consistent earnings, which at the midpoint of their expectations would represent nearly 5% growth over last year. Their restructuring will very likely finish by year end, leaving them leaner and more capable of taking advantage of any positive shift in end-consumer purchasing behavior.

Why a Put Option?

We don’t really want to increase the position in LEG unless it becomes absurd not to. If LEG were to fall to $7.50 per share and come in at the low end of their guidance, the result would be a P/E ratio of 7.5 and shares yielding 2.7%. With an average P/E ratio of over 17 and a historically low P/E ratio of 7.46 at the end of 2025Q1, there is probably no better point at which to be assigned for a turnaround candidate such as LEG. That price point of $7.50 also just happens to be an available strike price.

Let’s keep in mind LEG just traded above $10 on multiple days prior to the earnings announcement. From peak to trough in the week surrounding the announcement, we’re talking about a 25% sell-off from $10.60 to $7.86 as of the time of my trade recommendation and 17% of that drop came on the first trading day after the announcement. That’s absurd – and it is my assumption that it simply got caught up in the broader market panic brought on by tariff announcements.

Selling the put achieves two things:

- It brings in $50 in premium. I like to think of it as getting the one $0.05 dividend that will be declared and paid before the option’s expiry date of 2025-10-17 as if we actually owned the shares. The remaining $45 is equivalent to 3 x $15 which is like getting three $0.05 dividends for the 300 shares we already have! And of course, we will collect the $15 in dividends we would ordinarily collect (before 2025-10-17) on those 300 shares even if we never sold this put. This put pays for itself and gives us three quarters worth of dividends for the 300 shares we currently own.

- Selling at $8, there is only a 40% chance of assignment (personally, I think it is highly unlikely), but should assignment occur in the next 74 days, the average cost of the 400 shares after all dividends and option premiums would be at $12.54. This means, we would turn around on October 20th and sell four new call options with a strike of $12.50, collecting more premium for calls with a higher likelihood of assignment than otherwise possible with our previous profitable exit strike price of $15.00. Remember, we don’t want to see shares called away at a strike price that doesn’t produce a positive return on the position. This one put contract allows us to bring the strike price of covered calls down $2.50, from $15.00 to $12.501.

Worst case scenario, we spend a net $7002 to acquire 100 more shares, substantially reducing our practical exit-price point.

The most likely situation is that the put option will not be assigned, and neither will the 3 covered call options we sold with the same expiry date, i.e. the stock will remain range bound between $7.50 and $15.00.

Unlikely, but highly welcome: LEG climbs above $15 by 2025-10-17 and we see the put option expire worthless and our 300 shares called away, closing out the position with more green than we otherwise would have seen.

- The next lowest available strike price is $10.00. However, we would have to sell four $7.50 puts in order for their assignment to lower the average cost of the resulting 700 shares down to $10.00 per share. Royal Dividends does not wish to infuse $2,800 into a position we would like to exit as soon as it becomes profitable. At least, not yet. ↩︎

- Assignment for one contract means having 100 x $7.50 = $750 in the account in advance of the assignment, which for an American style option can happen at any point prior to and on the expiry date and is usually done when it is advantageous to the purchaser of the put, i.e. when the stock price is below the strike price. We collect $50 before commissions immediately upon sale of the put and this means the breakeven price of the put transaction itself is at $7.00, but make sure there is $750 in cash in the account, if not now, then as soon as you happen to see LEG dip below $7.50. If you cannot get $750 into the account, simply ignore this trade. ↩︎