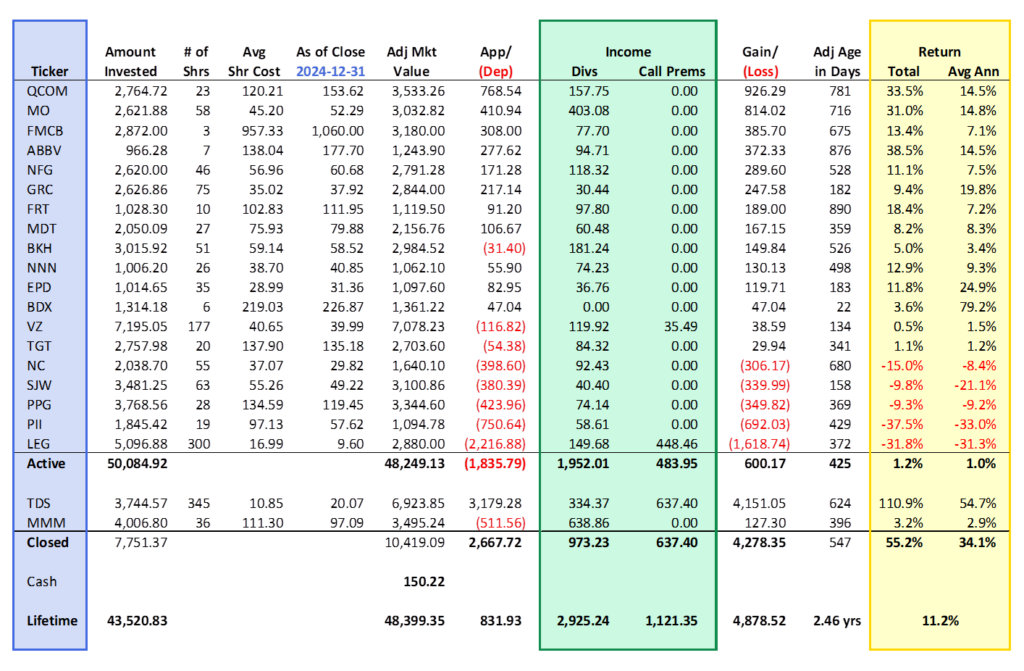

On 2024-12-31, the equally weighted S&P 500 Index [SPXEW] closed at $7,100.83, up 10.9% for the year excluding dividends. But it does include an atrocious -6.4% return in December. December’s performance is a reminder that account value, whether we like it or not, is transitory. Unrealized gains are just that, unrealized. Account value only becomes real when you cash in all your chips and get out of the game.

December turned a great year into a good year. Royal Dividends is still in the game and this quick update aims to focus on what is most important, dividends.

Once upon a time I thought that the Roundhill Investments S&P Dividend Monarchs ETF [KNGS] would be about the only ETF that could serve as an appropriate benchmark for the Portfolio for the Ages. Afterall, it was comprised solely of Dividend Kings. But alas, the fund is now defunct. I won’t use the market weighted S&P 500 Index [SPX] because the largest seven holdings (the ‘magnificent’ seven) makes up 33.8%. That is a poor match to the Portfolio for the Ages which has zero exposure to those companies. Frankly, it is a poor fit for measuring market performance in general, but no one is asking for my opinion.

I do use SPXEW, not really as a benchmark on which to compare performance results, but rather to speak of the market in general. Being equally weighted at least it gives a more balanced picture of the average performance of the 500 stocks that make it up.

Regardless of how the entire stock market performed in 2024, regardless of how one chooses to measure it, I am not happy with the performance of the Portfolio for the Ages. That does not mean it hasn’t performed well; it simply means that I desire better performance.

Observations

- Total return (includes realized and unrealized capital gains, dividends, and call premiums) is 11.2% since inception.

- Active holdings have an annualized total return of 1.0%.

- Fourteen of the 19 current holdings are in the black.

- Two holdings in particular, LEG and PII, have had appalling performance.

- LEG abdicated the throne this year and reduced their dividend. The position will be closed, but only after an honest attempt to get back to breakeven or better through capital appreciation, dividend income, and covered call premiums. This may take many more months.

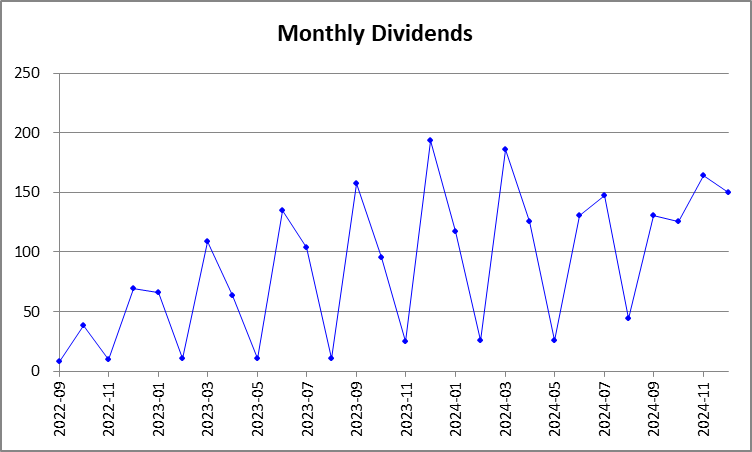

Those are just the observations from the chart above. What is unseen is the importance of dividends. LEG is the only stock that has failed to increase its dividend; the others continue their long streaks of annual increases in their dividend. The figure in the chart above indicates that Royal Dividends has received $2,925.24 in dividends since inception. However, this figure includes $449.74 in proceeds from the SOLV spinoff from MMM in 2024Q2. Taking a closer look at the $2,475.50 in pure dividends on a monthly basis, we see quite a bit of volatility, largely because I’ve made no effort to select companies based on the months in which they pay dividends.

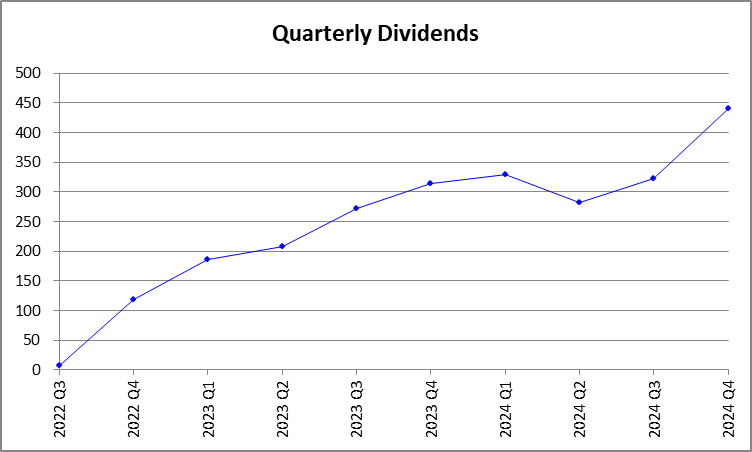

On a quarterly basis, we see a smoother picture.

LEG, MMM, and TDS all reduced their dividends early this year, and their collective impact is easily seen in the pronounced dip in 2024Q2. This was extraordinarily bad luck.

What else is easily seen? A quick recovery. This past quarter was the highest yet and I expect this to continue indefinitely. Account value will ebb and flow with the whims of the market forces and the vicissitudes of business for individual stocks, but dividends should only ever grow. Portfolio dividends will grow through four forces:

- With the exception of LEG, each stock has a long history of increasing their dividend each year, with an average streak of 45 years.

- Dividends are reinvested.

- Any capital gains from the sale of a position are reinvested.

- Each week sees another $250.00+ of outside money invested.

The companies raise their dividends per share (#1), and we raise the number of shares (#2, #3, and #4). This is how wealth is amassed.

When the market is confounding, focus on compounding.