This week, six of the portfolio holdings ranked in the Top 10: BDX, FMCB, HTO, PPG, QCOM, and SCL.

| Ticker | Account Value |

| BDX | 3,521.08 |

| FMCB | 4,060.00 |

| HTO | 3,062.43 |

| PPG | 3,246.60 |

| QCOM | 3,643.20 |

| SCL | 3,537.10 |

The lowest amount belongs to HTO. However, there exists a position and sector imbalance such that only FRT (position perspective) and Real Estate (sector perspective) are eligible for additional investment. Unfortunately, FRT nor any other Real Estate stock made the Top Ten. Upon relaxing the expected total return requirement from greater than 10% to greater than 9.3%, the first Real Estate stock makes an appearance at #24 in the expanded ranking. And it isn’t either of our current holdings, FRT or NNN.

It is time to add a new position to the Portfolio for the Ages!

UNIVERSAL HEALTH REALTY INCOME TRUST

Here is the profile from Schwab:

Universal Health Realty Income Trust, a real estate investment trust, invests in healthcare and human-service related facilities including acute care hospitals, behavioral health care hospitals, specialty facilities, medical/office buildings, free-standing emergency departments and childcare centers. We have investments in seventy-six properties located in twenty-one states.

Apparently, the logo is just the ticker symbol – I could not find an example of letterhead or any other communication that definitively displayed a more elaborate or imaginative logo. Also, nowhere mentioned in the profile or on UHT’s website is their relationship to another publicly traded company, Universal Health Services [UHS]. But I dig, I test.

There are three things of note concerning UHT’s relationship with UHS, but let us first take a quick look at UHS.

Here is the UHS profile from Schwab:

Universal Health Services, Inc., through its subsidiaries, owns and operates acute care hospitals, and outpatient and behavioral health care facilities. It operates through Acute Care Hospital Services and Behavioral Health Care Services segments. The company’s hospitals offer general and specialty surgery, internal medicine, obstetrics, emergency room care, radiology, oncology, diagnostic and coronary care, pediatric, pharmacy, and/or behavioral health services. It also provides commercial health insurance services; and various management services, including central purchasing, information services, finance and control systems, facilities planning, physician recruitment, administrative personnel management, marketing, and public relations services. The company was founded in 1978 and is headquartered in King of Prussia, Pennsylvania.

First, UHT got its start on 1986-12-24 by purchasing certain properties from subsidiaries of UHS and immediately leasing those properties back to the respective subsidiaries.

Second, UHS of Delaware, Inc., a wholly owned subsidiary of UHS, has been an ‘Advisor’ to UHT since the very beginning. The advisory agreement is renewed annually at the discretion of UHT, but it appears to be a formality.

Finally, the aggregate revenues generated from UHS-related tenants comprised approximately 40% of UHT’s 2024 revenue.

Suffice it to say, UHT goes as UHS goes. So how is UHS doing? I’ll be brief and use CFRA’s assessment on 2025-07-19 as representative of my own, admittedly brief, dive:

Our Buy recommendation reflects compelling valuation given strong business fundamentals and attractive EPS growth outlook. Recent results show improvements in volumes, staffing, and cost control. With 75% of supply chain protected from tariffs and stable wage costs supporting margins, we see continued operational strength. The behavioral health segment faces some near-term weather-related headwinds but maintains solid positioning.

CFRA’s 4-star ‘Buy’ rating carries a 12-month target of $205. With UHS trading at $155.60, there appears to be significant upside potential. Now, let’s examine UHT just a bit.

The Details

Data as of 2025-07-26

| Name | Universal Health Realty Income Trust |

| Ticker | UHT |

| Website | Investor Relations |

| Sector | Real Estate |

| Dividend Streak | 38 years |

| Last Price | $41.20 |

| Div Amt (quarterly) | $0.74 |

| Ann Dividend | $2.96 |

| Last Ann Div Inc | 1.4% |

| Dividend Yield | 7.2% |

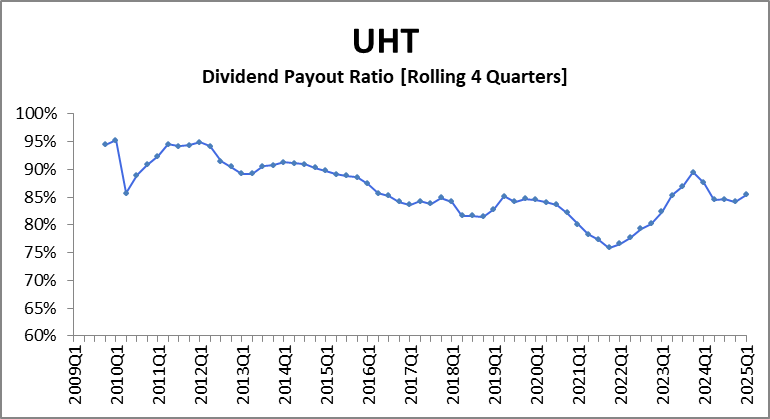

| Payout Ratio (ttm) | 85.7% |

| Beta (5-yr, mon) | 1.02 |

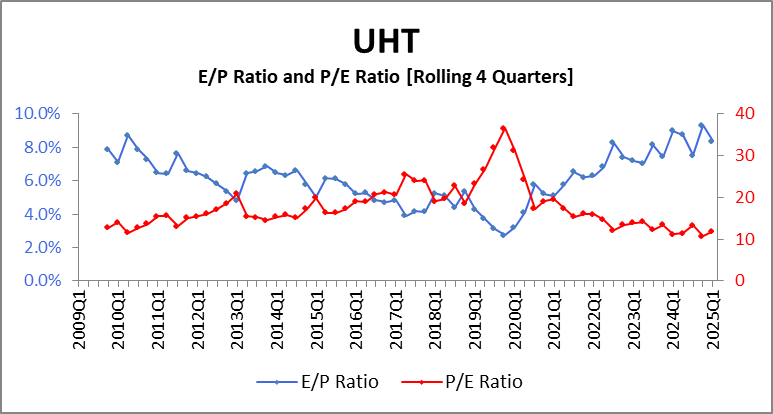

| P/E Ratio (ttm) | 12.01 |

| Margin of Safety | 6.8% |

Reasons to Invest

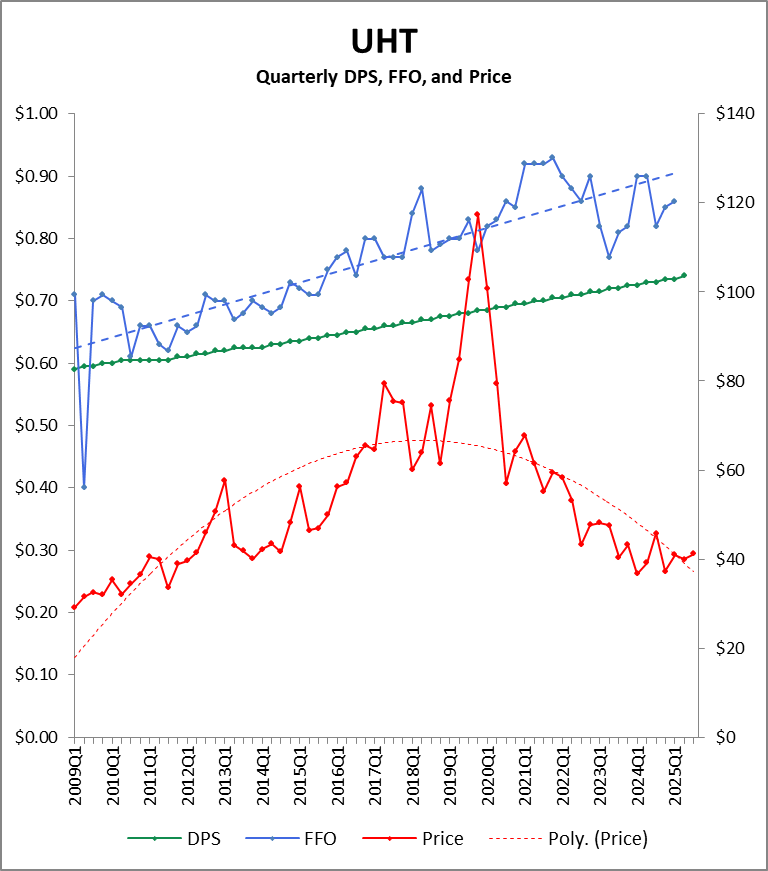

Quarterly earnings have flattened out since 2018, but the stock price is in a multi-year slide.

I don’t know why the stock memed its way past $100 back in late 2019 but now seems to have overcorrected. It is not common to see UHT trading as low as its current P/E ratio of 12.

Further, the dividend yield is a whopping 7.2% and is well supported by FFO.

Taking all of this into account the reasons to invest are rather straightforward: This investment is all about boosting our weighting in Real Estate via the one REIT in the Royal Dividends Empire that is most deserving at this time (it edged out Realty Income Corportation [O] by the slightest of margins). It’s a slow earnings grower but is slightly undervalued and pays a massive dividend.

Additionally, UHT possesses a large portfolio of specialized healthcare facilities. Unlike traditional office or retail assets, which face headwinds in a shifting economy, these healthcare-focused properties serve as a resilient hedge against volatility. As America’s population ages and demand for medical services rises, facilities such as sub-acute care centers and outpatient surgery suites are likely to remain essential infrastructure in the nation’s care continuum.

I will be acquiring 24 shares of UHT on Monday morning. Let us hope for a strong earnings announcement after market close on Wednesday.