This week, seven of the portfolio holdings ranked in the Top Ten.

| Ticker | Account Value |

| BDX | 3,395.49 |

| CMCSA | 946.39 |

| FMCB | 4,044.00 |

| HTO | 3,191.25 |

| PEP | 1,899.17 |

| PPG | 3,225.75 |

| SCL | 2,947.80 |

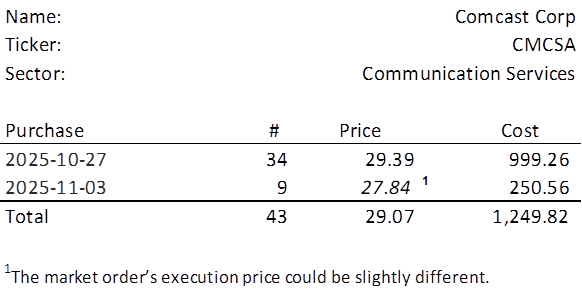

The lowest amount belongs to CMCSA which last traded at $27.84. Therefore, I will acquire 9 shares on Monday. Below, is the purchase history and average cost calculation.

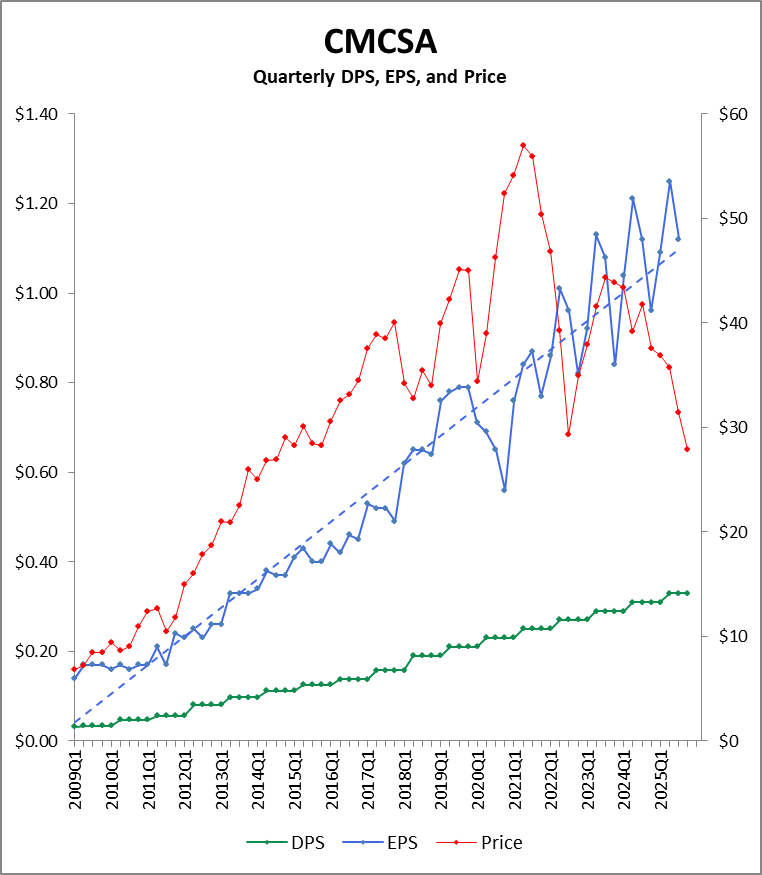

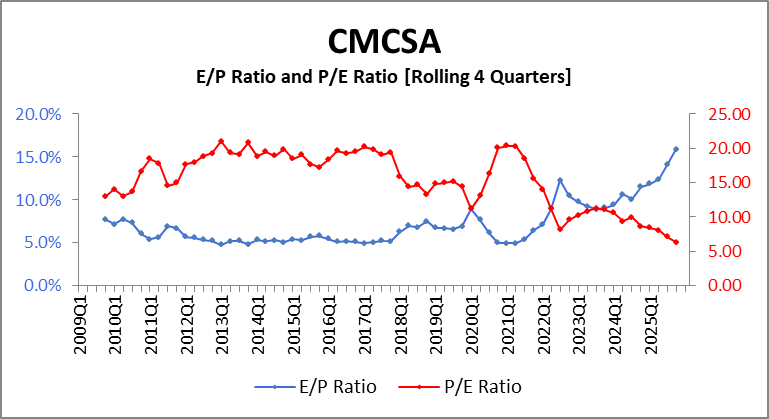

CMCSA announced quarterly earnings just a couple of days ago and just a couple of days after we opened a position. May as well place this recent performance in the context of the last 16+ years.

Observations

Stock Price

CMCSA is in a 50-month price slide, down 55% from its all-time high of $61.80.

Personally, I felt that getting CMCSA under $30.00 was about the best one could hope for, but the market seems far more interested in providing an even bigger discount at $25.00. I wouldn’t rule out a sell-off down to $15.00. Of course, it wouldn’t necessarily be warranted, but Wall Street isn’t exactly tethered to reality.

Those two price levels above are just two more examples of ‘magnetic’ price levels established far too long ago to be thought of as having any impact whatsoever, but that I am convinced do have an impact. These price levels aren’t the same as ‘support’ from a technical analysis perspective, though quite often they’re the same magnitude. Support refers to a price level where a stock tends to stop falling because buying interest at that price is strong enough to reverse course. But the initial downward price movement could simply be the everyday drifting we call ‘participation in a broader market sell-off’, a superficial overreaction to headline news, or a mindless, algorithmically driven response to an ill-conceived, unprovoked tweet.

A magnetic price level is more active. Long thought to be dead, it is a malevolent and ancient energy, an unseen force that actively pulls the stock toward it like gravity or, well, like a magnet. The stock has no choice but to reach that level.

How does a stock eventually overcome that dark energy and bounce off the magnetic floor like a spring that explodes after the force of compression is removed? Love. Really.

There are thousands of publicly traded companies, and the truth is that only a subset of companies that deserve focus, attention, and investment receive their due at any one time. Sometimes the set of stocks getting the love is so small it is akin to a radio station that plays the same 60 songs all day, every day. It isn’t until a collective overexposure causes disgust and perhaps an allergic reaction that we see the masses turn their attention towards something different, a deeper cut if you will.

Of course, it is possible to approach the magnet at such a velocity that a stock goes right through it to the other side. Sadly, the other side of the magnet pushes away. It repulses. Then the stock can look forward to feeling the attraction of an even greater evil still…a lower price point.

With that in mind, let’s take a very superficial look at the earnings that were announced this past week.

Earnings

Magnitude/Trend

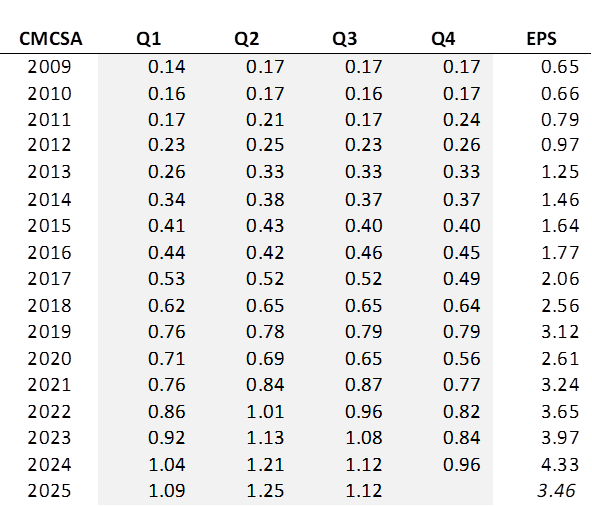

For the one thousandth time, the market, with absolutely zero public information was able to sense what would be a lackluster quarter after an excellent streak of earnings. 2025Q3 EPS of $1.12 was a decrease from 2025Q2 as would be seasonally expected but was identical to 2024Q2 EPS. The first half of the year had seen an increase of 4% over the same period in the prior year, and so this Q3 result indicates a slowing down.

Seasonality

Typically, the quarterly distribution of annual earnings breaks down as follows: 23.8% in Q1, 26.2% in Q2, 25.3% in Q3, and 24.7% in Q4. In other words, there is virtually no seasonality to the earnings. Even each half is 50%. The slight drop-off from Q2 to Q3 has been increasing over the last few years.

CY2025 EPS is highly likely to be the best ever but could simultaneously represent low single digit growth over 2024.

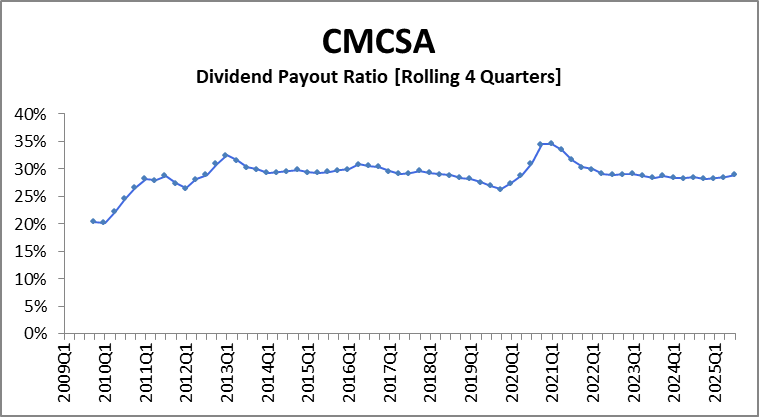

Dividends

With a streak of just 17 years of dividend increases, we cannot be certain of the dividend’s resiliency should things turn sour. How reticent to reducing, suspending, or even cutting the dividend altogether might management be should there be a significant downturn in the American economy? We don’t know. But we do know that it is safe now and things would have to deteriorate significantly before CMCSA would likely consider doing anything stronger than, say, an increase of just $0.01 or even less per quarter.

Thoughts on Investment

Sure, the market seemed to indicate that future growth in earnings would crater and that we just had our first indication CMCSA has officially jumped the shark coming in with no improvement over the prior year. This was the first time a quarterly EPS announcement hadn’t broken a record for that particular quarter in fourteen consecutive quarters! Royal D knows how to time ’em people!

The trailing 12-month P/E ratio currently sits at 6.3—a record low over its historical range. Meanwhile, the earnings ratio has never been higher. The market is pricing in a flatline (or worse) in earnings growth that defies the underlying fundamentals and the still observable trend. But because the P/E ratio is so ridiculous, so downright immature, I cannot help but think the price will fall to $25. Because if 6.3 isn’t objectionable, would 5.6 raise any eyebrows?

The price behavior reflects investor concerns over future relevance of cable and broadband services. But that perspective ignores just how low CMCSA is valued right now and a good company’s ability to make adjustments going forward.

It is a good time to add some shares and if we ever do get this position up to a round lot, CMCSA would be a great stock on which to write covered calls and increase our income from the position.