2025-02-01

This week, three of the portfolio holdings ranked in the Top Ten: FMCB, PPG, and SJW.

| Ticker | Account Value |

| FMCB | 3,120.00 |

| PPG | 3,230.64 |

| SJW | 3,164.49 |

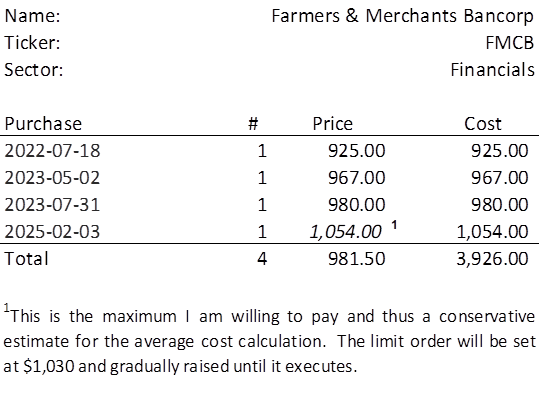

The lowest amount belongs to FMCB which last traded at $1,040.00. I will acquire 1 share of FMCB on Monday. Below, is the purchase history and average cost calculation.

Let’s touch upon a number of areas. First up, FMCB.

FMCB

There is an outstanding limit order to acquire one share for $975. It has been working for a couple of weeks, and it has not executed. FMCB did trade as low as $990 on two consecutive days, 2025-01-14 and 2025-01-15. However, their earnings announcement on 2025-01-22 was excellent and while I would love to grab a share for under $1,000, it may no longer be in the cards.

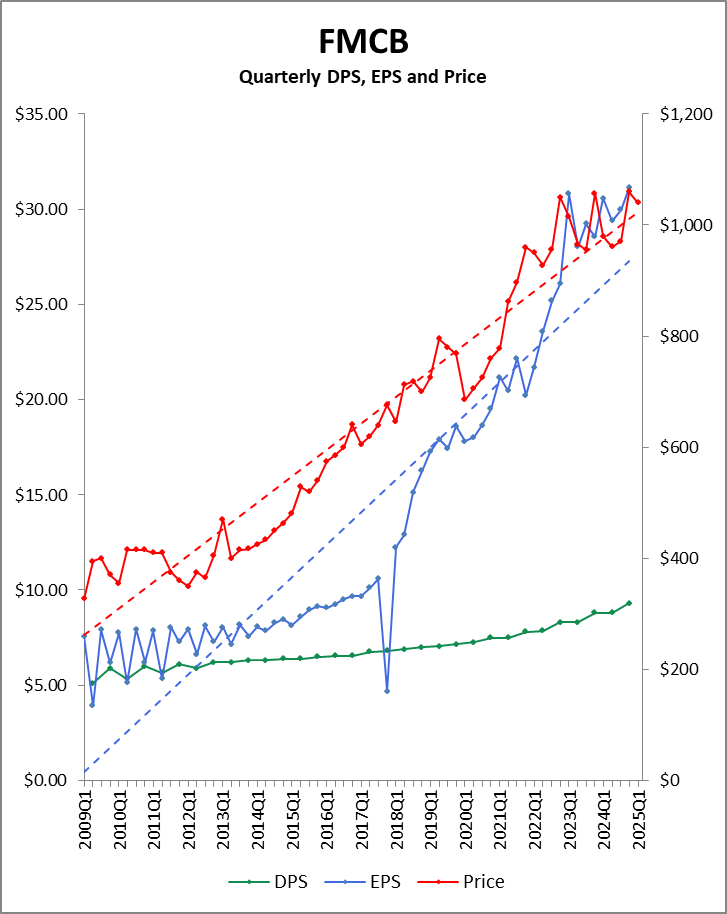

As you can see in the chart above, the idea for stealing a share for $975 was not without merit; there had been a strong prevalence for FMCB to settle down nearly as quickly as it would spike up. It happened again, but it just didn’t come down as far as I had hoped.

FMCB would still be the recommended purchase of the week if it had last traded as high as $1,054.00. Above that, the recommendation would have been SJW, another company I will be addressing in this post. Thus, I will be changing the existing limit order’s execution price from $975.00 to $1,030.00, and will gradually increase the limit, until the order executes. I will go no higher than $1,054.00

Since it has been a year and a half since we last invested in FMCB, let’s take a look at its recent performance in the context of the past 16 years.

Observations

- Each of the last three quarters have been record-setting quarters (the best ever Q2, the best ever Q3, and the best ever Q4. The CY2024 EPS was a record $121.02, up from $116.61 from the prior year, an increase of 3.78%

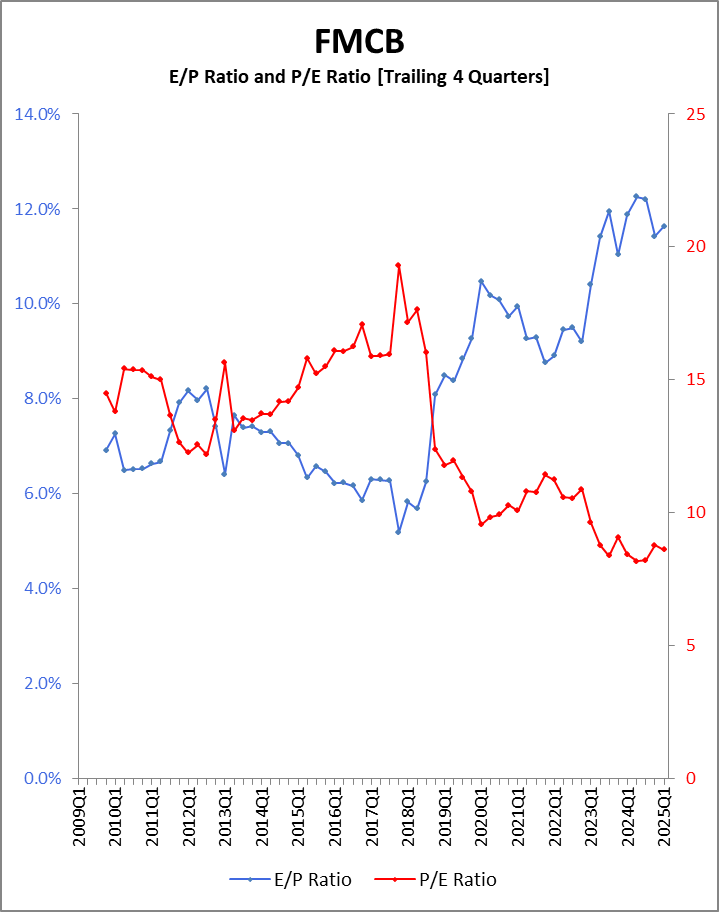

- Price growth has essentially stalled and there is visible ‘multiple compression’. Meaning the P/E Ratio has been coming down. This can be seen in the disappearance of the gap between the red line and blue line. Or, if you would rather see it more explicitly shown, take a look at this chart.

- The past 16 years can really be looked at as two periods. Prior to 2019, FMCB oscillated around a P/E Ratio of about 15. Since then, it has fallen off with an average under 10 and more recently trading around a P/E Ratio of 8.5.

- Ironically, FMCB traded at higher multiples when it had slow-growing, very consistent earnings, but now that earnings have taken off, the stock is trading like the stodgy bank it once was.

- With a payout ratio of 15%, the divided is extraordinarily well covered. Increases should continue for the foreseeable future.

Folks, it is a great time to grab more FMCB.

PII

On the other end of the earnings spectrum, we have PII.

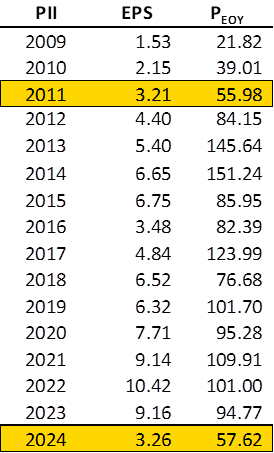

Fourth quarter earnings came in a little better than expected, but expectations were low. CY2024 EPS of $3.26 is a throw-back to 2011 and the price at the end of 2024 was remarkably similar to 2011 too. Unfortunately, the price has come down quite a bit in January, both before the earnings announcement and after as well. I suppose the reason is that while $3.21 was all very nice and wonderful when it was a significant increase over the previous year and even better years lay ahead. But with the memory of record earnings still fresh, $3.26 is depressing, and don’t get me started on the 2025 guidance of $1.10 EPS.

The good news is that PII just raised its dividend for the 30th consecutive year. The press release has very typical, positive language, but I found the earnings call from a few days before to be more informative and I present it here as an example of what a company thinks about at least at a high level and puts into a somewhat off-the-cuff response to a good question.

Craig Kennison, Analyst, Baird: Yes. Thanks. And thanks, Bob. I’m wondering, Bob, maybe on the dividend, I know it’s important to you, you’ve got the aristocrat status. But if I look, I mean, earnings are going to be well under half of the dividend payment in 2025. So maybe just help us bridge that gap and help us understand the levers you can pull to generate the cash to get to your 30th consecutive year of dividend growth?

Bob Mack, Chief Financial Officer, Polaris: Sure. Yes, look, I think, as we talked about earlier, I think we feel good about our free cash flow for 2025. Obviously, we have looked at the dividend. The yield is pretty attractive right now for investors. And as Mike and I were on the road, I guess late November, early December, we got a lot of feedback from some newer investors that they were looking for their entry point or had found their entry point and they liked the dividend yield because they felt like it gave them protection and a good stream of income while we’re waiting for the industry to recover.

So we didn’t want to make a sudden change. We believe this is short term in nature. We got through the dealer inventory, the bulk of it in 2024. Obviously, we’ll have to manage a little bit depending on what happens in the market in 2025. In 2025, we’re dealing with the knock on effect of that with our build being lower than our ship to get finished goods inventory right and drive cash. And we feel like it makes sense to use that cash to continue to pay the dividend, because we do see, as Mike said, customers are still riding their products. We’re not seeing people leave the industry. We’re not seeing a glut of used products in the market. So it’s not that people aren’t riding, it’s just this delayed replacement cycle, particularly in the recreational focused products. And we think that’s going to continue to get better as consumers work through their balance sheets over the next couple of years. And so we don’t want to make a sudden change to the dividend that then sort of takes us off the track we’ve been on for a long time based on a 1-year dynamic, which is similar to the decision we got during COVID. We felt like that was short term and unlike a lot of companies, we continued our dividend and that turned out to be the right decision. So that’s where we are here, too.

Now, PII may still be trading at $47.70, but, and the market doesn’t want to admit this yet, the price will continue to fall until the power sports business starts to pick up. How far will it fall you ask? When it gets to $37.00.

At around that point, I expect the market to realize that its culture of abuse is excessive and uncalled for. That’s when I see the stock price bouncing at least a little. PII is in a very cyclical business and when things turn around for the industry, PII will actually be in really good shape to take advantage of that upturn. Now, what makes me think that once PII trades down to approximately $37.00 that it will bounce and not continue to fall? Well, another Royal Dividends position in the red.

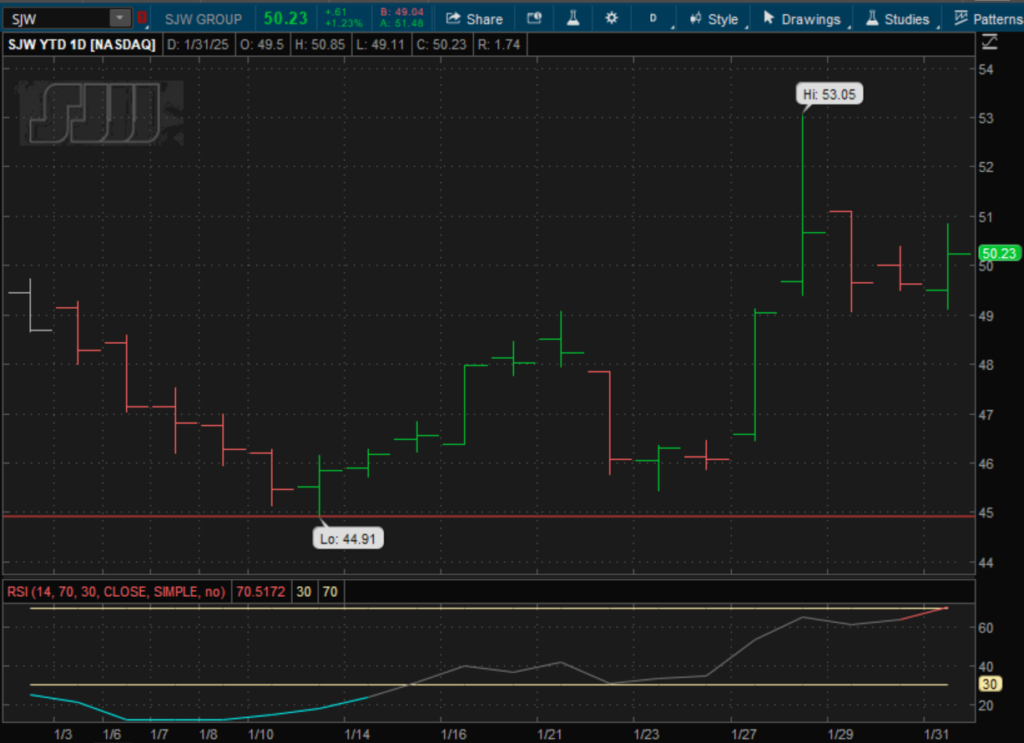

SJW

The market is better at remembering the past than it is at predicting the future. Of course, that would have to be true. But you get my point. Royal Dividends holding SJW just respected a price point that it first hit back in late 2006 and then used as support in 2017 and then again during the throes of Coviddery in early 2020.

On the monthly chart below it is easy to see how SJW touched that point and we can see from the price label to the right (and above) that it has bounced up to $50.23.

Here is what the bounce looked like upon zooming in.

SJW is not out of the woods, but the zoom allows us to see that it was, at least initially, a pretty strong bounce, 18% from a low of $44.91 to a high of $53.05.

Think about that. There were perhaps thousands of individuals who saw SJW pivot on 2024-01-13 and wondered why. There was no earnings announcement before or after, and nothing newsworthy. Most would have assumed that it was simply because the broader market reversed on that day. Still others might have thought that it was simply an attractive entry point for a great company.

But one individual says it is because 18 years ago, the market remembered the excitement and promise of SJW. It remembered falling in love and feverishly pushing SJW to a price point of $45.00, a price point that it wasn’t quite ready for. Timing is everything after all. It would be a decade before they hooked up again and this time it was for good. Sure, there are misunderstandings. And the market does have a roving eye, chasing after bobby-dazzlers. But just when you think things might be over for good, it remembers what is real.

Water and dividends are real.