This week is the second of three ‘off’ weeks intended to restore the $250+ per week pace of investment. This is necessary because a new position was established in ADP. But guess what – there’s $665.11 of cash available for deployment, so let’s carry on, shall we?

This week, six of the portfolio holdings ranked in the Top Ten.

| Ticker | Account Value |

| ADP | 925.44 |

| HTO | 3,613.53 |

| PEP | 3,921.27 |

| PPG | 4,174.83 |

| QCOM | 3,158.82 |

| VZ | 7,865.87 |

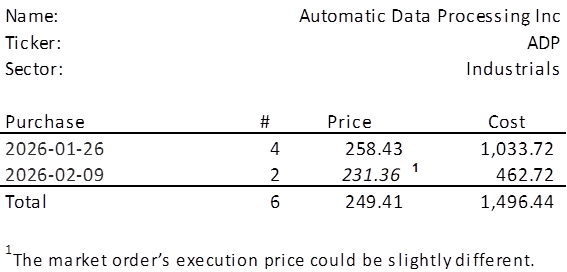

The lowest amount belongs to ADP. This is very fortunate, because there is a position imbalance whereby the only position eligible for additional investment is in fact, ADP. Let’s grab 2 shares of ADP on Monday morning and we will still count this as an off week because we don’t need to reach into our pockets to make the purchase. Below, is the purchase history and average cost calculation.

ADP announced quarterly earnings on 2026-01-28, just two days after we opened our position. Let’s see how this recent performance falls into the context of the last 17+ years.

Observations

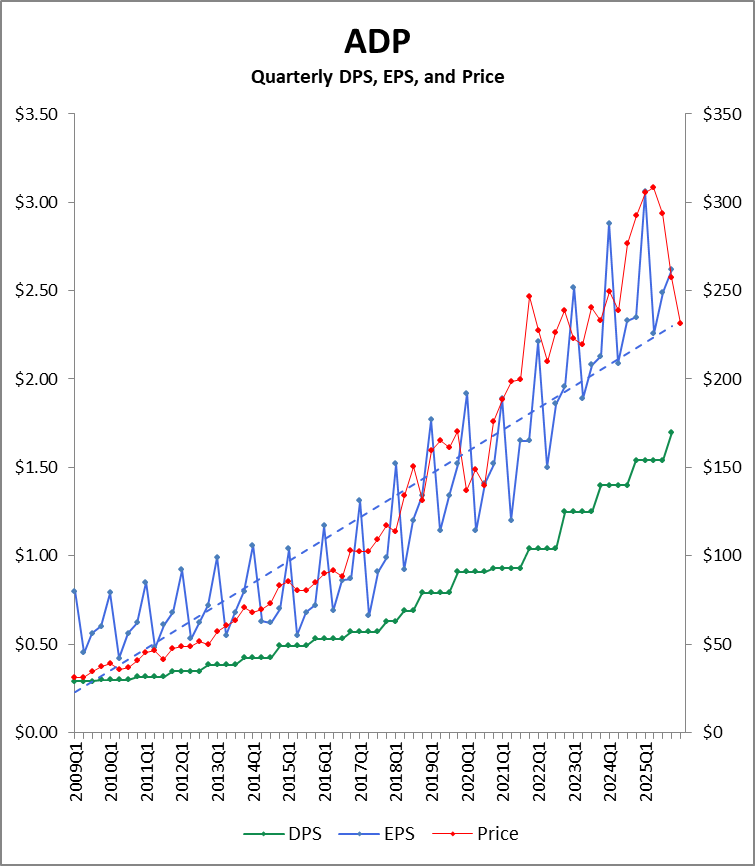

Stock Price

ADP dropped from an all-time high of $329.93 on 2025-06-06 to $231.36 on 2026-02-06. Shedding 30% in eight months is surprising for a company whose earnings are climbing steadily.

I do not believe the reasons for this decline are specific to ADP but rather macroeconomic in nature. In short, ADP benefits when hiring is strong, wage growth is strong and interest rates are high (because they earn ‘float’ income on client funds placed in their care). However, over the last eight months, hiring has cooled, wage growth has moderated, and expectations of further rate cuts by the Fed translates into reduced future income from the investment of those client funds.

Earnings

Magnitude/Trend

Clearly, the quarterly earnings are in a strong, long-term, positive trend. The blue dotted line in the chart above actually does a decent job of delineating the overall earnings trend, even if the variation about that linear trend line is both significant and seasonal in nature.

Seasonality

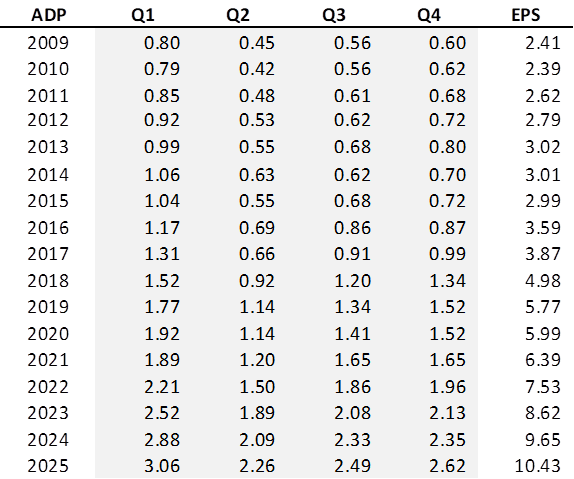

Typically, the quarterly distribution of annual earnings breaks down as follows: 31.9% in Q1, 19.3% in Q2, 23.5% in Q3, and 25.3% in Q4. The variation around these percentages is minimal and are reliable.

CY2025 EPS was a record high and 2025Q4 EPS were the best Q4 ever. In fact, there have been 19 straight quarters where we could say that. But it would appear the market has little hope that earnings can keep growing.

Dividends

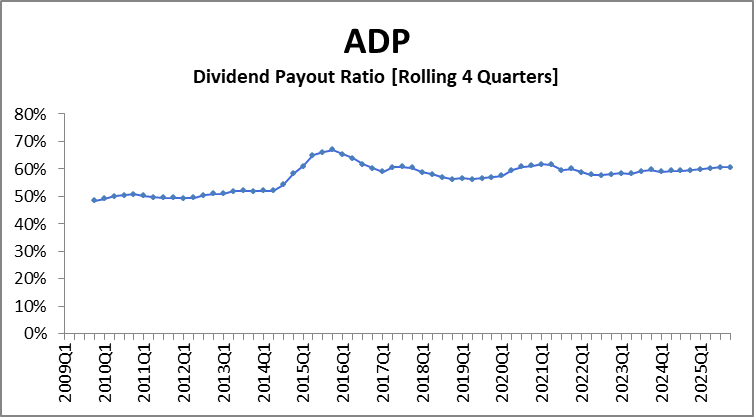

ADP is a Dividend King, with an impressive 51-year streak of annual dividend increases. The company’s dividend payout ratio has been steadily trending higher. Ordinarily, a rising payout ratio relative to earnings per share (EPS) could raise concerns about the sustainability of future dividend growth. Yet, ADP’s earnings are remarkably consistent from quarter to quarter, allowing the company to comfortably support a higher payout ratio. Furthermore, the payout ratio is still at a comfortable 61%.

Thoughts on Investment

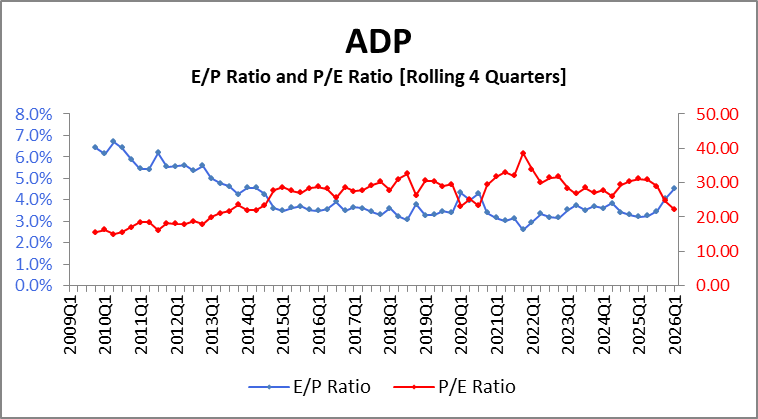

The trailing 12-month P/E ratio currently sits at 22.8, lower than the average of 25.9 over the period above.

I don’t know what the fair value of ADP is, but I am quite certain that it is trading below fair value as I type. I am also certain that it cannot keep dropping every time the quarterly earnings set a record for that quarter.

Despite the current administration’s insistence that the labor market is thriving, the actual pace of job creation has been strikingly weak — and the irony is hard to miss. ADP, whose payroll data often becomes the nation’s primary employment gauge whenever federal reports are delayed or disrupted, has been quietly documenting this slowdown month after month. In other words, the very act of sidelining official government statistics doesn’t change the underlying reality: the private‑sector experts who keep payrolls running can still see that job growth has been close to nonexistent.

If you want proof that the market trusts ADP’s numbers, just look at the chart above: the stock’s recent pullback and compressed P/E aren’t signs of doubt — they’re signs that investors take ADP’s payroll data seriously enough to reprice the business when job growth stalls. The irony, of course, is that ADP has every incentive to paint a rosier picture of the labor market, since stronger employment would almost certainly lift its own share price. Yet the company continues to report what the data actually show, even when the truth is inconvenient.

That kind of integrity doesn’t just build credibility — it creates opportunity. And right now, it’s an excellent moment to accumulate shares.