I was about 35 years old when I finally caved in and got myself some glasses. I hate wearing glasses, but not because of how they look. It’s the constant pushing them back up my nose. It’s the irritation above the ears from the constant use. Before I needed bifocals, I certainly had the option of buying contact lenses, but I chose not to. They cost more than glasses – and I already disliked having to spend any money at all on the matter.

In the 1960s, the cost of replacing a pair of contact lenses was about $200. Many of the younger cohort inclined to wear contact lenses found this replacement cost to be prohibitive. But of course, the cost wasn’t about to stop them from choosing contact lenses over glasses and so, contact lens insurance was born. One of the first contact lens insurers was founded by Gerald D. Stephens in 1965 and it became one of the largest of its kind in the United States.

Over time, the demand for the insurance diminished with the emergence of more affordable, disposable soft lenses. In order to remain competitive, Stephens began offering other types of insurance, including commercial property and liability insurance. The company eventually got out of the contract lens insurance line altogether and thrives in the property and casualty industry today. In fact, on 2025-02-13, they announced a dividend increase making this the 50th straight year of doing so. We have ourselves another Dividend King in the Royal Dividends Empire.

All hail RLI Corp!

My Eyes is Going Crazy

Technically, the ‘RLI’ in RLI Corp [RLI] stands for Replacement Lens Incorporated, but you won’t find that on their website. In fact, I couldn’t find any of the company’s history on the official site – I thought my eyesight was going. Perhaps they’re just very focused on the now. Fair enough, let’s see what they’re up to.

According to Charles Schwab:

RLI Corp., an insurance holding company, underwrites property and casualty insurance. Its Casualty segment provides commercial and personal coverage products; and general liability products, such as coverage for third-party liability of commercial insureds, including manufacturers, contractors, apartments, and mercantile. It also offers coverages for security guards and environmental liability for underground storage tanks, contractors and asbestos, and environmental remediation specialists; and professional liability coverages for errors and omission coverage for small to medium-sized design, technical, computer, and miscellaneous professionals. This segment provides commercial automobile liability and physical damage insurance to local, intermediate and long haul truckers, public transportation entities, and other types of specialty commercial automobile risks; incidental and related insurance coverages; inland marine coverages; management liability coverages, such as directors and officers liability insurance, fiduciary liability and coverages, employment practice liability, and for various classes of risks, including public and private businesses; and home business insurance products. The company’s Property segment offers commercial property, cargo, hull, protection and indemnity, marine liability, inland marine, homeowners’ and dwelling fire, and other property insurance products. Its Surety segment offers commercial surety bonds for medium to large-sized businesses; small bonds for businesses and individuals; and bonds for small to medium-sized contractors. The company also engages in various reinsurance coverages. It markets its products through branch offices, wholesale and retail brokers, carrier partners, and underwriting and independent agents. RLI Corp. was incorporated in 1965 and is headquartered in Peoria, Illinois.

From the summary at the bottom of their own press release(s):

“All of RLI’s subsidiaries are rated A+ “Superior” by AM Best Company. RLI has paid and increased regular dividends for 50 consecutive years and delivered underwriting profits for 29 consecutive years.”

They are very good at what they do.

RLI becomes the 6th Dividend King from the Financials sector. Below is a list of all the Kings in the Financials sector and the industry in which they conduct their business.

| Company | Ticker | Industry |

| Commerce Bancshares Inc | CBSH | Banks |

| Cincinnati Financial Corp | CINF | Insurance |

| Farmers & Merchants Bancorp | FMCB | Banks |

| RLI Corp | RLI | Insurance |

| S&P Global Inc | SPGI | Capital Markets |

| United Bankshares Inc | UBSI | Banks |

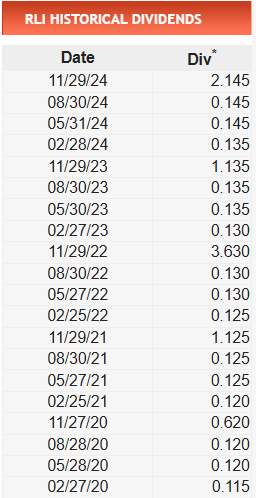

RLI just declared a 2:1 stock split on 2025-01-16 and then on 2025-02-13, declared a $0.15 quarterly dividend to be paid on 2025-03-20. That would imply an annual dividend of $0.60, and a very low yield of (0.60/74.54) = 0.8%. However, RLI has followed a pattern of a low first quarter dividend followed by three higher dividends and in recent years, the fourth quarter dividend is augmented by a large special dividend. The last five calendar years of dividends are shown on a split adjusted basis in the table below (courtesy DividendChannel.com).

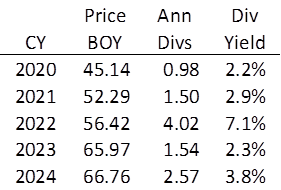

Now, special dividends are not considered in the calculations that determine the dividend streak of a company, but they are very real and in the case of RLI, substantial. Below is the price of RLI at the beginning of the last five calendar years and the total dividends paid that year.

The effective dividend yield is actually substantial and the price appreciation nothing to sneeze at either. Who knows? One day RLI may find itself in the Portfolio for the Ages.