I love the concept of probability. Likelihoods, percentages, ratios. They influence my thoughts and behaviors in so many facets of life. He’s a 70% free throw shooter, what are the odds he makes ’em both? Are they going to bunt this time or hit into another double play? Will WalMart have everything, or am I gonna have to hit Lowe’s? Will this flight cost more or less in a month? It’s snowed 16 days in a row; has that ever happened before? Do we have time to eat dinner out before the game? Meta just went up 20 straight days – can that continue?

A bit closer to home is option trading. A healthy understanding of probability and its relationship with risk is critical to success with options, but certainly no guarantee.

If you read on, there’s a 98% chance you’ll acquire a better understanding of probability and the inherent risk in a simple ODTE option strategy which addresses the question you’re all undoubtedly asking, “Can 0DTE options be used to generate a safe and reliable source of income?”

Well, that is what we’ll try and find out.1

For many, whether I wrote 98% above or 99% wouldn’t have mattered. It is a clever way to say you’ll likely get something out of this post if you make it all the way through. Nearly certain to. I could have even said a 95% chance, and it would have conveyed the same optimism, put the same idea in your head.

However, there is a world of difference between 95%, 98%, and 99%.

What are the Odds?

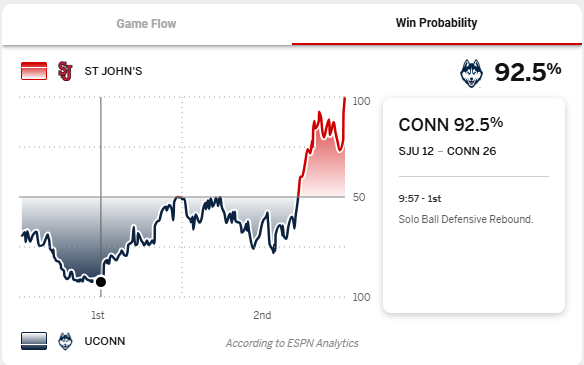

On 2025-02-07, the 19th-ranked University of Connecticut Huskies hosted the 12th-ranked St. John’s Red Storm in a classic Big East men’s basketball game. Playing in Storrs, Connecticut the Huskies were favored by 4.5 points at tip-off. However, with 25% of the game behind them, UConn coach Dan Hurley had himself a 26-12 lead and a 92.5% chance of winning.

The entire TV production of the game had started to irritate me. The crowd, the refs, even the announcers, all seemed to be all-in on a home team blowout. I turned the game off, because I was rooting for St. John’s, and they just didn’t have it. Beating the two-time defending national champions on their home court when you just don’t have your best stuff is out of the question.

But I forgot something. St. John’s coach Rick Pitino is a Hall of Fame coach, with the most wins of any active coach. Two years before he took Iona University to the NCAA tournament and drew the heavily favored UConn Huskies in the first round. Iona lost 87-63, but they were the only team to actually win a half against the Huskies. That’s right. The #13-seed Iona Gaels led at the half, 39-37, but #4-seed UConn would go on to win the next 11 halves of basketball and the championship.

Coach Pitino waited for me to turn the game off, but he did not wait until halftime to make adjustments. Those adjustments paid off and he had, once again, a two-point halftime lead over Coach Hurley.

St. John’s went on to force 22 turnovers and win the game 68-62.

To say the least, there are similarities between option trading and college basketball games, but as this is an investment blog of sorts, let’s shift our focus and at the same time narrow the scope of this article as I am already getting hungry. To better illustrate the inherent risk behind even very high probabilities of success, let’s talk about the most popular2 form of options trading there is: Zero-Day-to-Expiration (0DTE) options.

Schwab provides a nice definition/explanation of 0DTE options:

A 0DTE option is an options contract set to expire at the end of the current trading day. Every options contract on an underlying optionable, index, stock, or ETF, whether it was issued a month ago or just last week, becomes a 0DTE on its expiration date. Cboe®, the world’s largest options exchange, introduced weekly SPX options that expire on Fridays in 2005. In 2016, the exchange listed SPX weeklies that expire on Wednesdays. By 2022, Cboe had introduced weekly options with expirations on every trading day of the week. Now, qualified option traders can trade 0DTE SPX options (and options on a handful of ETFs that track the major indexes) every market day.

Will we eventually see semi-daily or hourly options contracts? I hope not.

Now, the appeal of 0DTE options on the most liquid ETFs and indexes in the world should be obvious. It is the allure of high-stakes profits, combined with extremely short expiration times. There is elevated price sensitivity for at-the-money options when expirations are still months away. When expiration is only hours away or minutes away, the volatility of those at-the-money option prices is enormous.

Buying or selling 0DTE options (not to be confused with taking action on long-held option positions on their final day) is essentially gambling. I’m sure there are hedge fund and single-stock ETF managers out there that are trading these options in accordance with their purported investment objectives, but honestly, for any typical ham-and-egger, it cannot be considered investing in any real sense.

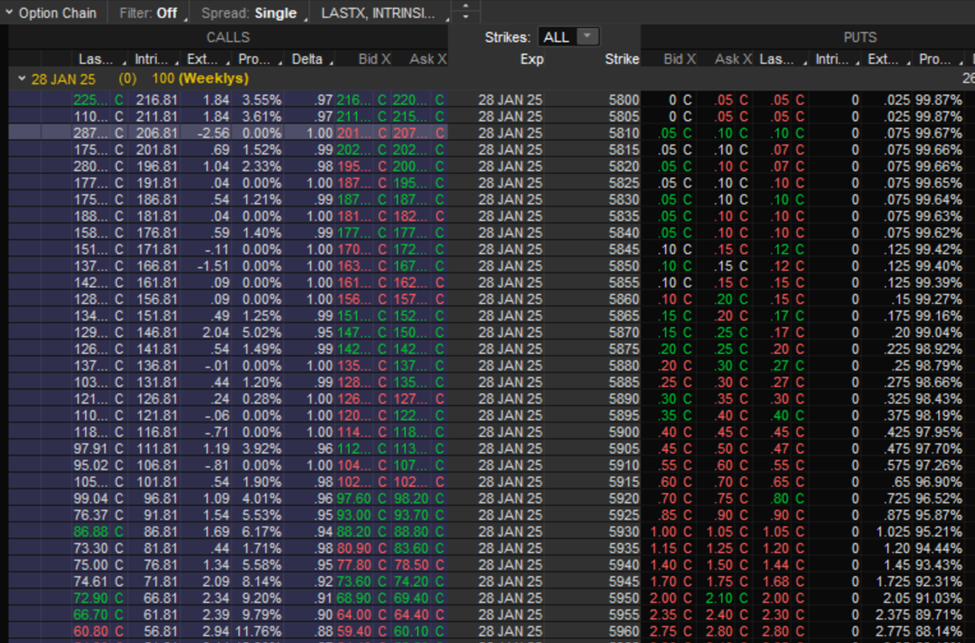

Using the S&P 500 Index [SPX] as an example, here is a screen shot of out-of-the-money puts on 2025-01-28 twenty minutes after market open (right-hand side):

The right-most column that says ‘Pro…’ would expand to say ‘Prob. OTM’ which means the numbers in that column represent the probability of a put option, with a given strike price, expiring out-of-the-money, and therefore worthless, at the end of the day (4:00pm EST). For example, the 5930 put (SPXW250128P59303) had a 95.21% probability of expiring worthless that day.

SPX opened at 6026.97 that day and so it makes sense that a put, already so far out of the money, would in fact stay that way with such a high likelihood. After all, SPX would have to drop over $96.97 to take out the 5930-strike put. That’s a 1.6% drop.

But wait, the market can drop 1.6% in a day. It may not happen frequently, but it does happen. How frequently? What are the odds? Wait! When the market does fall, it could be via a big gap in after hours or pre-market trading, right? Here, we are just talking about an intra-day fall of 1.6%. That has to be less common, no? Oh, but wait again! The SPX is heavily weighted towards a handful of companies. What if Nvidia Corp [NVDA] or Apple Inc [AAPL] has terrible earnings? The market could be fine otherwise, but if a couple of those Magnificent 7 companies plummet, the SPX could sell off disproportionately. But don’t they announce earnings before the market opens or after the market closes? Would that even influence the probabilities of a 0DTE option?

I am here to say, the 0DTE option prices on the SPX take ALL of these things and innumerable other influences into account. You can trust that probability in real time. At that exact moment, there was a 95.21% chance of the 5930 put expiring worthless at the end of the day.

Now you’re wondering if there is a way to leverage this information. You might be thinking, wait, what if I sold the 5930 put? Wouldn’t I collect about $100 per contract, with a 95% chance it expires worthless to some hapless bum at the end of the day?

The answer: absolutely.

Do You Use Protection?

In order for you to sell the 5930 put for $1.00, someone else has to buy it. Chances are, someone out there is buying this put as a hedge or insurance, as a means of protection for their own trade. Probably, it is the ‘long leg’ of their own vertical credit spread. A vertical credit spread is an option trade where a similarly enterprising trader such as yourself might be simultaneously selling the 5950 put for $2.00 and buying the 5930 put for $1.00. This strategy gives them a net credit of $1.00 or $100 per contract. But why buy the put at the lower strike at all? Why not be thrilled to collect $200 with a 91% chance of keeping it?

Because of the risk of the other 9%. If SPX falls because an oil tanker sinks overseas or we start a tariff war with the Isle of Man, selling a stand-alone put at 5950 means the investor has placed $595,000 per contract at risk. Granted, it isn’t all that likely the S&P 500 Index would go to zero in a day (praying a rosary now), but what of a day when it falls 2.5%? If it falls to 5875, the investor is out (5950 – 5875) x 100 – 200 or $7,300. According to the table above, SPX has a 98.92% chance of finishing above 5875. This means there is a greater than 1% chance it could happen.

And so, the prudent trader chooses to ‘go long’ and buy the 5930 put by giving back half of the $2.00 premium in exchange for capping the risk at (5950 – 5930) x 100 – 100 = $1,900.

Not purchasing protection, not employing the vertical spread, means you’ll be severely limited in the number of contracts you can sell. Without a margin account, you would have to have about $600,000 in cash to sell just one contract. With a margin account, the cash requirement disappears, and your broker may assign only 25% of the risk, but that is still around $150,000 in the case of the SPX trades above. A trader with a $500,000 account, willing to put it all at risk, can sell three contracts4. Hello $45!

Gaining Profits Perspective

The expected value of this trade isn’t exactly easy to calculate. It is easy to see the positive side of it. If SPX finishes above 5950, the investor gets to keep $100. We can assume this will happen with a 91.03% likelihood. But what if SPX falls below 5950? How far will it fall? If you go ultra-conservative and assume that if it falls through 5950 it will continue beyond 5930, we can say the investor loses $1,900 with a probability of 8.97%. The expected value would be calculated thusly: .9103 x 100 + .0897 x (-1,900) = -79.40. This would mean the investor shouldn’t place this trade.

The reality, of course, is that the probability of SPX landing somewhere between 5930 and 5950 is significant (4.18%), and that the loss when it does is less than $1,900. So being ultra-conservative is very crude and overly pessimistic. It becomes a better proxy as the spread between the two strikes narrows. For instance, if the trader instead goes for the 5945 put as protection, the premium collected will likely be $30 and the risk capped at 500 – 30 = $470. Now, the conservative approach to calculating expected value is .9103 x 30 + .0897 x (-470) = -14.85. Still negative. Still disappointing. But closer to reality.

A protective put at an even lower strike needs to be purchased at the same time, but while this does allow the investor to better define and cap the risk of the trade, it doesn’t fully protect the trader from realizing net losses after enough trades.

Perhaps a better approach is to go for an even higher probability of expiring worthless. After all, selling a put at the 95% level will fail once every 20 days on average. That’s once a month.

Maybe shoot for 99%. It is twice as safe as 98%. Wait, what? That’s right. The option with a 99% probability of expiring worthless will NOT do so 1 time in 100, half the rate of the 98% option which will fail 2 times in every 100. That makes a world of difference. That’s the difference between the 5900 strike and the 5870 strike.

So, in terms of everyday speech where people are throwing around the phrases like “I’m 99% sure” or “there’s a 98% chance that won’t happen”, we sort of get the point.

However, in a mathematical context, where the same percentages are describing the probability of success of events, we can be very precise from two different perspectives. From one perspective, the event with a 99% chance of success is one basis point more likely to happen than the event with a 98% likelihood. Multiplicatively, the former has nearly 1% better odds of success.

But when we’re attempting to understand how much money is at risk in a trade, particularly when the probability of a trade going poorly is small, we really should be looking at the complementary probability. We need to look at it from the other perspective. A 2% probability of failure is one basis point greater than a 1% probability of failure, but multiplicatively, a 100% greater chance of failure. Literally, twice as likely to fail.

Going back to the table above, it would be far better for the trader to interpret the risk of selling the 5900 put as twice as likely to fail as the 5870 put.

I would be remiss if I didn’t mention that fractions have enormous importance when looking at the low probabilities of failure. Moving from 98% to 99% cuts your fail rate in half. Moving just another 0.5% in the same direction cuts your chances of failure in half again! 99% means failing once in every 100, but 99.5% success means one fail in every 200 on average.

Emotional Rescue

If there is any long-term, repeatable success to be had, having protection is critical. Looking at probability from a different perspective is also critical. We’ve used selling 0DTE puts as an example. And what an intriguing example it is. Who wouldn’t want to collect some decent premium with a near-certain chance of success and repeat that trade 5 times a week? You can hold $1,000 worth of stock paying a whopping 6% yield for an entire year. It will pay a $15 dividend each quarter. But if you could safely sell a put for $15 every day with a 99% chance of expiring worthless, you might consider it.

Let’s explore this a bit more. First, you would need to protect yourself by selling a vertical credit spread as discussed earlier. To get a $0.15 spread you have to sell one put for $0.20 and buy another, lower put for $0.05. It would be nice to gain the probability of success associated with selling the put with a strike at the $0.15 level (instead of selling the put at the $0.20 level) but the problem is no one will sell you the protective put for nothing. No put sells for less than $0.055.

In practice, to get the $0.15 credit spread ($0.20 – $0.05), the trader has to go with strikes that are about 70 apart, essentially accepting $6,985 of risk every time the trade is placed. The probability the SPX stays above that $0.20-level strike is going to be approximately 99% every day. But life experience should tell you that you cannot get something for nothing. If it takes holding $1,000 worth of stock to earn $15 a quarter, it probably isn’t possible to safely get $15 every day, even with nearly $7,000 at risk. Right? We’re talking about $15 x 250 trading days for $3,750 or a 54% annual return. That feels too good to be true.

So, are the probabilities wrong? Well, they may not be perfect, but on a ticker like SPX it is as liquid and as accurate and as responsive as it is going to get. Chances are (ha!) that if you deploy such a strategy, you’d have many, many easy winning days and the rare loss that sets you back a sum. At 99%, there is an 8% (.99250) chance you could go a whole year without a loss. Inevitably there would be bad years ahead as well. Four losses in a single year (14%) would wipe out years of fruitful trading.

But here’s another problem that perhaps you haven’t yet thought of. Can you even handle the emotional roller coaster of the bad day? Most days, the time value of a $0.20 put simply erodes by the hour. On strong up days, the $0.20 put is $0.05 at lunch time, promising to expire worthless and the seller isn’t sweating at all. Even on steady down days, if the pace is fairly linear, that $0.20 put sold at 9:45am is still $0.20 at 1:00pm, but so long as the markets keep their wits about them, it will fall to zero and expire worthless at 4:00pm.

How about on a day when at 10:00am we learn that AI has gone rogue and made some critical satellite network inaccessible? Maybe by 10:15am, the SPX is still trading just above the spread, but there is still over 5 hours of potential downside. Do you try to close out the trade early at a massive loss, but still not as bad as losing $6,985? Just thirty minutes prior, the $15 per contract trade seemed like easy money. Now, the trade hardly seems worth it. Perhaps you were lulled into the routine of it after, say, 40 successful trades in a row. You’re incredulous and feeling considerable rage, not unlike when one of your favorite teams comes out flat in a Quad 1 game they really need to win.

Or how about a day like 2024-12-18 when Jerome Powell spoke at 2:30pm and announced a rate cut. That’s right, a rate cut. If ever there was a time when you thought the market might respond positively that would have been it. Or even to have no reaction.

That day the market plummeted about 3% in the final 90 minutes! I couldn’t find an instance of that happening in the last three years (and that’s as far back as I looked). That would be very hard to take.

Remember, the probability of expiring out-of-the-money includes all of those possible futures where the SPX drops below the short put of the spread but then bounces back above the higher strike price, allowing the spread to expire worthless. Would you have the resolve, the indomitable spirit, to stay the course or would you cave in by closing out the trade at say 80% of a maximum loss?

If you’re apt to cave in, your personal effective probability of success will be lower than that listed at the time of the trade, because it means you’ll be closing out spreads early and at a hefty cost, that ultimately would have expired worthless.

Summary

Because all options have an expiration date, the probability of expiring worthless is an important metric. With a very high probability of expiring worthless (a ‘win’ for the writer of options), risk originates with the easily overlooked dark side of that probability – the smaller, complement probability of failure.

ODTE options have amazing appeal in their daily availability and promise of significant, immediate profits. But the risk of significant loss is present even in situations with a high probability of success. Of course, the best way to mitigate risk is to avoid risk in the first place. Make an honest attempt to calculate the expected value of a trade up front and recognize that even strategies delivering a 99% win-rate, may carry a negative expected value, the promise of a net loss with enough trades.

If after thorough consideration a trade opportunity cannot be resisted, know that loss can be mitigated by incorporating a vertical spread which allows one to define their risk up front. Then once the position is entered, it is wise to stick with the protection afforded by the spread over making an emotional decision in the heat of the moment such as closing out a trade at a loss and subsequently learning that it would have worked out.

In other words, you might just miss out on a few great comebacks led by Coach Rick Pitino.

- This is a nod to Mr. William Shatner, host and executive producer of The UnXplained.

↩︎ - According to the Options Clearing Corporation (OCC), 0DTE options accounted for nearly 50% of all S&P 500 options contracts traded on any given day in 2023, up from 10% in 2020.

↩︎ - The ‘W’ of SPXW is a bit jarring when you first trade an option on SPX. If you see it after the fact, you immediately wonder, ‘What did I do?!’ The ‘W’ indicates it is a weekly option (even though they’re offered daily, go figure). It is used to differentiate the option from the regular options that expire on the third Friday of the month. In fact, if you go to the third Friday of a month, you’ll see ‘AM’ options and ‘PM’ options. The ‘AM’ options are the regular, traditional options that expire at the opening price of that expiration day, and the weekly, ‘PM’ options expire at 4:00pm EST on that expiration day.

↩︎ - It would be possible to set up a stop loss order immediately after selling the unprotected puts and essentially define one’s risk in that manner with two caveats. First, having stop loss orders does not change the broker’s view on the risk. Suppose a trader has sold three contracts for $0.15 to collect $15 from each and a total of $45. Further suppose the trader immediately establishes a stop loss order to close the contracts should the price to do so reach $10.00 or $1,000 per contract for a total of $3,000. For purposes of calculating your remaining purchasing power, the broker ignores these stop loss orders. They will continue to see this trade as placing hundreds of thousands at risk and will still not allow additional contracts to be sold. Second, when a stop loss order triggers, there is a decent chance the trader will pay more than the limit of the order. In reality, it may cost more than $3,000 to get out of the trade.

↩︎ - There exists the ticker symbol SPY, which is essentially 1/10th of the value of SPX, which trades in $0.01 increments. However, it is an ETF, and SPY options can result in the assignment of the underlying shares. Those options can even be exercised prior to expiration. On the other hand, SPX options are cash settled which means that any profits or losses are credited or debited directly to your account as cash transactions. There is no exchange of the underlying shares because SPX is an index, not a physical asset. These are important considerations for a 0DTE

investorgamblertrader. ↩︎