Along with the usual $250+ weekly contribution, we have $296.85 in uninvested cash available to deploy.

This week, six of the portfolio holdings ranked in the Top 10.

| Ticker | Account Value |

| ADP | 3,830.27 |

| BDX | 2,952.60 |

| HTO | 4,010.97 |

| PEP | 3,463.11 |

| PPG | 3,556.74 |

| SCL | 3,540.76 |

The lowest amount belongs to BDX. However, if we were to acquire any shares of BDX it would create a position imbalance whereby only UHT would be eligible for additional investment. Unfortunately, UHT is not ranked in the Top 10. That can only mean one thing.

It is time to add a new position to the Portfolio for the Ages!

Marzetti Co

Here is the profile from Schwab:

The Marzetti Company engages in manufacturing and marketing of specialty food products for the retail and foodservice channels in the United States. It operates in two segments, Retail and Foodservice. The company offers frozen garlic breads under the New York Bakery brand; frozen Parkerhouse style yeast and dinner rolls under the Sister Schubert’s brand; salad dressings under the Marzetti, Cardini’s, Marzetti Simply, and Girard’s brands; vegetable and fruit dips under the Marzetti brand; croutons and salad toppings under the New York Bakery, Chatham Village, and Marzetti brands; and frozen pasta under the Marzetti Frozen Pasta brand. It also manufactures and sells various products to brand license agreements, including Olive Garden dressings, Buffalo Wild Wings sauces, Chick-fil-A sauces and dressing, Texas Roadhouse steak sauces and frozen rolls, and Subway sauces. The company sells its products through sales personnel, food brokers, and distributors to retailers and restaurants. The Marzetti Company was formerly known as Lancaster Colony Corporation and changed its name to The Marzetti Company in June 2025. The company was founded in 1896 and is based in Westerville, Ohio.

Obviously, the logo is unremarkable and so we move on.

If you’re ever eaten food, you’ve very likely eaten something made by Marzetti.

The Details

Data as of 2026-05-24:

| Name | Marzetti Co |

| Ticker | MZTI |

| Website | Investor Relations |

| Sector | Consumer Staples |

| Dividend Streak | 63 years |

| Last Price | $115.00 |

| Div Amt (quarterly) | $1.00 |

| Ann Dividend | $4.00 |

| Last Ann Div Inc | 5.4% |

| Dividend Yield | 3.5% |

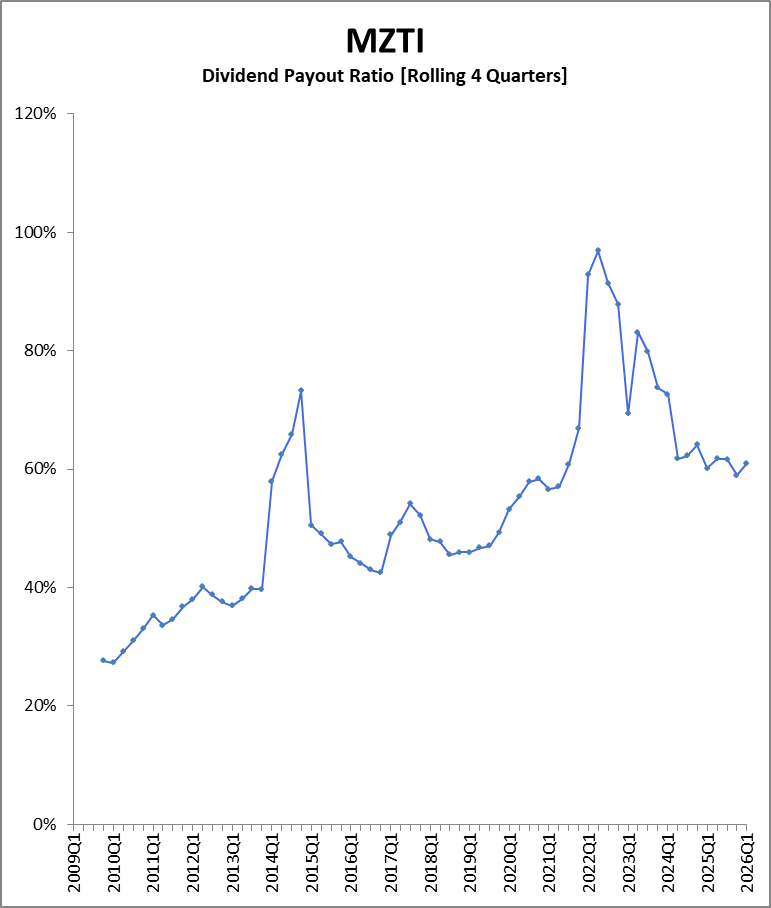

| Payout Ratio (ttm) | 61.0% |

| Beta (5-yr, mon) | 0.38 |

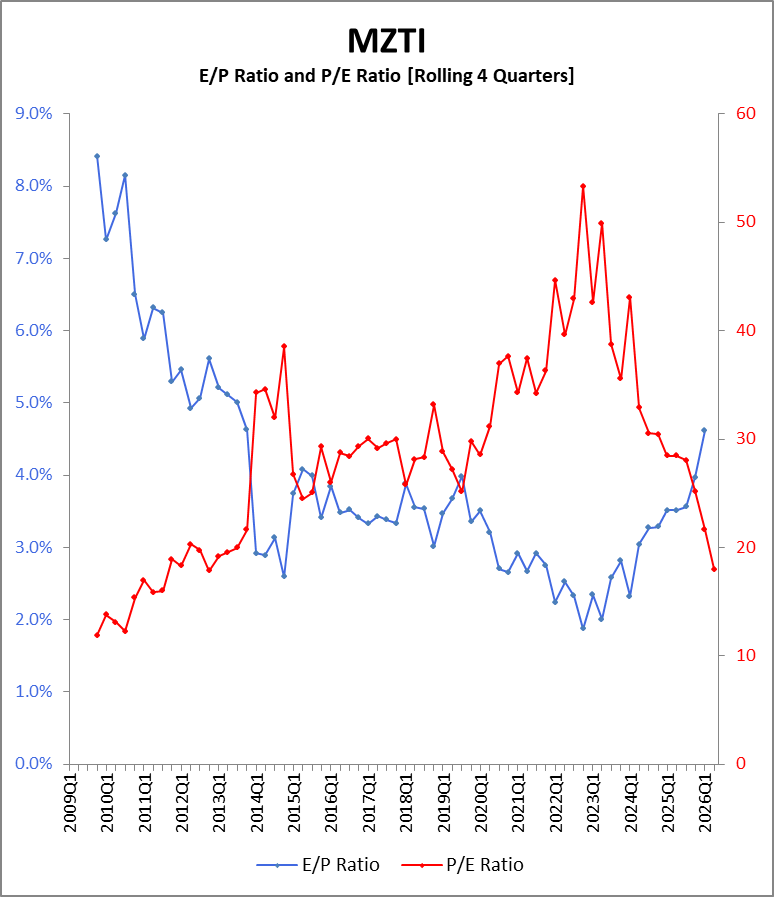

| P/E Ratio (ttm) | 18.00 |

Reasons to Invest

MZTI reached an all-time high of $220.65 on 2023-05-05. It has dropped 48% since then and 75% of that decline (3500 basis points) has occurred since 2026-02-02. Why has it dropped so much? I think because dreams of this consumer staple company being a growth company have finally died. Honestly, as you’ll see in the charts below, it isn’t obvious as to why MZTI has traded at the multiples it has in the past. But as to why the 3-year price decline has been accelerating, I think there are several reasons:

- 2026Q1 EPS of $1.35 missed estimates by $0.22

- Retail weakness due to inflationary policies

- Debt was taken on to acquire Bachan’s, Inc., a Japanese BBQ sauce brand

- Oversized packaging of a certain Chick‑fil‑A sauce resulted in a forecasting error

- Loss of management credibility largely related to #4

- Investigations/shareholder probes largely brought on by #4

Let me just expand on #4 because it is a great example of just how easily a stock selloff is triggered. Buried in the question-and-answer section of the earnings call transcript is the CEO David Ciesinski’s response to an analyst’s question as to the cause of some ‘friction’ in the ‘club channel’:

So within club, two different points of noise, one is we’re lapping the launch of Chick-fil-A sauce last year, so we had a big pipeline build in the period. When we went out with that item, we launched it in a two-pack, so two 20-ounce Chick-fil-A sauce.

What we found is that the sell-through was strong, however, buyers didn’t come back, and when we did the math, what we realized is that we were selling consumers about what becomes a year’s worth of supply of Chick-fil-A sauce. So in conversations with the buyers at Chick-fil-A, what we’ve elected to do is to come back with a three-pack, so it’s going to be two smaller originals and one Polynesian sauce, and that’s shipping into the marketplace now.

Now you might have heard that and thought nearly nothing of it. But many a nervous nelly thought differently. Let me clarify. The CEO is talking about club‑channel retail (Costco/Sam’s), where a household would have purchased a twin‑pack of 20‑oz bottles. A typical serving of sauce is roughly 1–2 ounces, and most households don’t use Chick‑fil‑A sauce every day. Probably once a week or even less. This is how buying a twin-pack, 40 ounces of sauce, might last many months or even a year.

Believe it or not, this hiccup cost the stock as much as 7%!

It’s a funny thing really. A company like Facebook can change its name to Meta and go all-in on the ‘metaverse’ only to get off that train a couple of years later, and still find itself thriving as one of the Magnificent Seven. But a Dividend King that sells refrigerated dressings and sauces makes a packaging/shipping mistake on one product in one retail sales channel and shareholders seek reparations via the typical class action lawsuits (and there are always law firms looking to help).

Obviously, this is more about management credibility than it is about too much sauce. In the end, the oversupply wasn’t a sign of strong demand, but a sign that the company had misread demand and now has prior sales which will appear inflated and it will make future quarters look weaker by comparison. This undoubtedly affected forecasting and budgeting as well.

But let’s calm down for crying outloud.

I believe MZTI is oversold and this disrespect has created a wonderful opportunity and I’m not the only one who thinks MZTI is undervalued.

GuruFocus has a fair value of $183.

Sure Dividend has a fair value of $189.

Personally, I am doubtful that MZTI will return to those levels any time soon. That might happen if the successful completion of the acquisition of Bachan’s, announced on 2026-05-01, starts to produce the growth for which they were purchased.

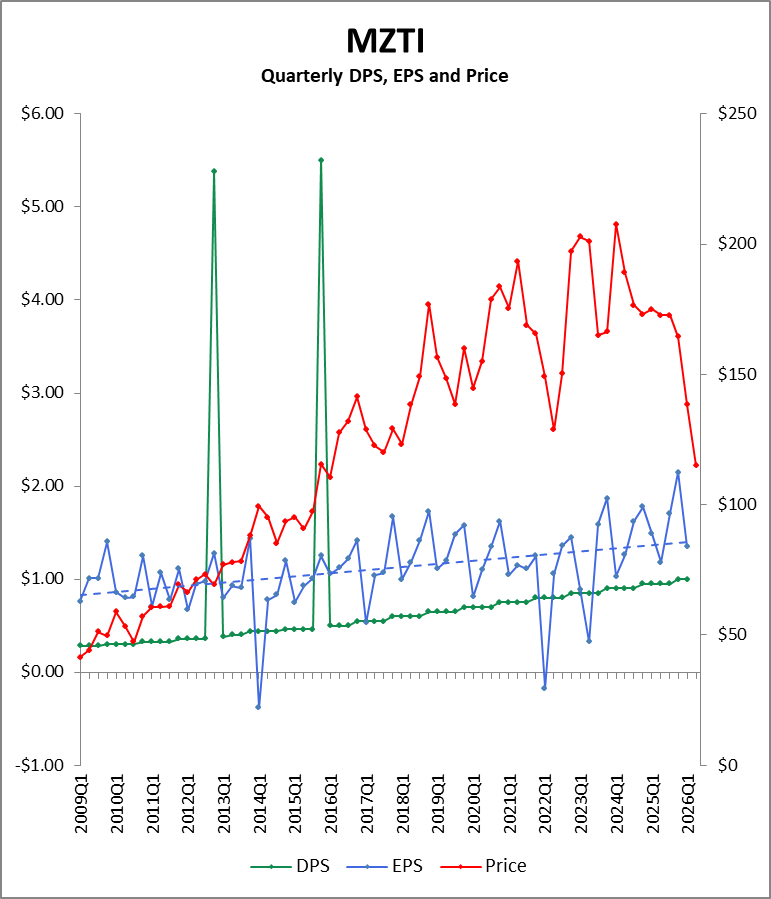

First, note the two spikes in the dividend stream. In addition to the regular cash dividend, a $5 special dividend was paid twice, three years apart. Second, note the long-term trend in earnings as indicated by the dashed blue line. There is certainly a seasonal volatility about that line, but the slope is not a dramatic one. It is the slope you might expect of a slow-growing Dividend King. Yet the price up until three years ago was skyrocketing on expectations, trading at multiples over 40 even the years following the pandemic.

The current P/E ratio of 18 is by no means laughably low, but it is hard to find a bottom with these types of situations. It could certainly go lower, but I would like to point out that while the 2026Q1 EPS of $1.35 was a $0.22 miss on estimates, and lower than 2025Q1 EPS of $1.49, that $1.49 was the best Q1 ever – so it isn’t so terrible that MZTI didn’t top that quarter1. AND the quarter once removed, 2025Q4, had EPS of $2.15, a record for any quarter!

It’s as if the market’s expectations from 6 years ago are finally coming to fruition, but it got tired of waiting and spent all its money on Micron [MU].

I’ve removed the effects of the two special dividend payments of $5 each in the chart above. With those removed, we can see the payout ratio has been very slowly climbing for the last 17 years, and has spiked the two times MZTI lost money in a quarter. But the steadily rising divided has never been unaffordable. The payout ratio reached the high 90s four years ago, but it rests just above 60% right now.

MZTI has 63 years of dividend increases and the current dividend is well-covered.

Let’s hope this misstep is behind them and the EPS growth trend continues.

Royal Dividends will initiate its position with 11 shares of MZTI on Tuesday morning, supported by our standard $1,000 allocation and the $296.85 cash balance. (Markets are closed Monday for Memorial Day.)

- The Chick-fil-A sauce misttep is at least one factor behind both the record first quarter from a year ago and the magnitude of the earnings miss this quarter. The mistake undoubtedly inflated the EPS of $1.49 and caused estimates for this past quarter to be an inappropriately high $1.57. Investors in consumer staples companies want predictability and this problem threw a wrench into the works. I know one thing; customers will come back for that sauce. On a recent trip to New York City, I availed myself of Chick-fil-A twice on the New York State thruway and the quality of their food and customer service is unmatched in the fast food industry.

MZTI’s fiscal year ends on June 30th. But it is worth mentioning that the EPS of the first calendar quarter (the third quarter of their fiscal year) has demonstrated 4 times the volatility of the other three quarters. The only two times in the past 17 years EPS was negative for a quarter was in the first calendar quarter of the year. This could also be a factor that helps explain the earnings ‘miss’. It isn’t difficult to imagine the last two first quarters of $1.49 EPS and a $1.35 EPS playing out in a different manner had the great over-saucing not occurred, perhaps with Q1 EPS of $1.42 each year. Then investors would have focused more on the lack of revenue growth and seen it in a more isolated way. Certainly, they would have punished the stock for that reason, but it might not have been as dramatic. ↩︎