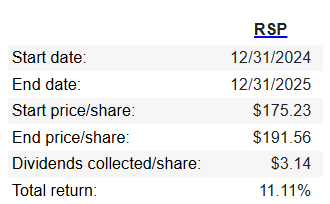

On 2025-12-31, the equally weighted S&P 500 Index [SPXEW] closed at 7,763.92, up 9.3% for the year excluding dividends. To assess the performance with dividends, it is convenient to look at the total return of the Invesco S&P 500 Equal Weight ETF [RSP].

The dividends yielded 1.8%. The real question: How did the Portfolio for the Ages do?

Let’s examine some easily ascertained facts and see if we can’t estimate the 2025 return for the Portfolio for the Ages:

A) value of the portfolio at market close 2024-12-31: 48,399.35

B) value of the portfolio at market close 2025-12-31: 70,936.96

C) external funds contributed in 2025: 15,296.63

D) dividends received in 2025: 2,235.68

P) option premiums received in 2025: 546.94

Now B = A + C + D + P + G, where G equals the amount of unrealized gain or loss.

G = B – A – C – D – P = 70,936.96 – 48,399.35 – 15,296.63 – 2,235.68 – 546.94 = 4,458.36

Because new money is regularly added in approximately equal amounts throughout the year, let’s make the simplifying assumption that all of the contributions to the fund were made halfway through the year on July 1, 2025.

The 2025 return (i) for the Portfolio for the Ages is as follows:

i = (D+P+G)/(A+.5C) = (2,235.68 + 546.94 + 4,458.36) / (48,399.35 + .5*15,296.63) = .129

A one-year total return of 12.9% is great performance and I am pleased with it. The dividends yielded 4% and option premium brought in another 1%. The nearly 8% of unrealized gains (there were no realized gains from sale of stock in 2025) is the transitory component of account value and return – unrealized gains, after all, are unrealized.

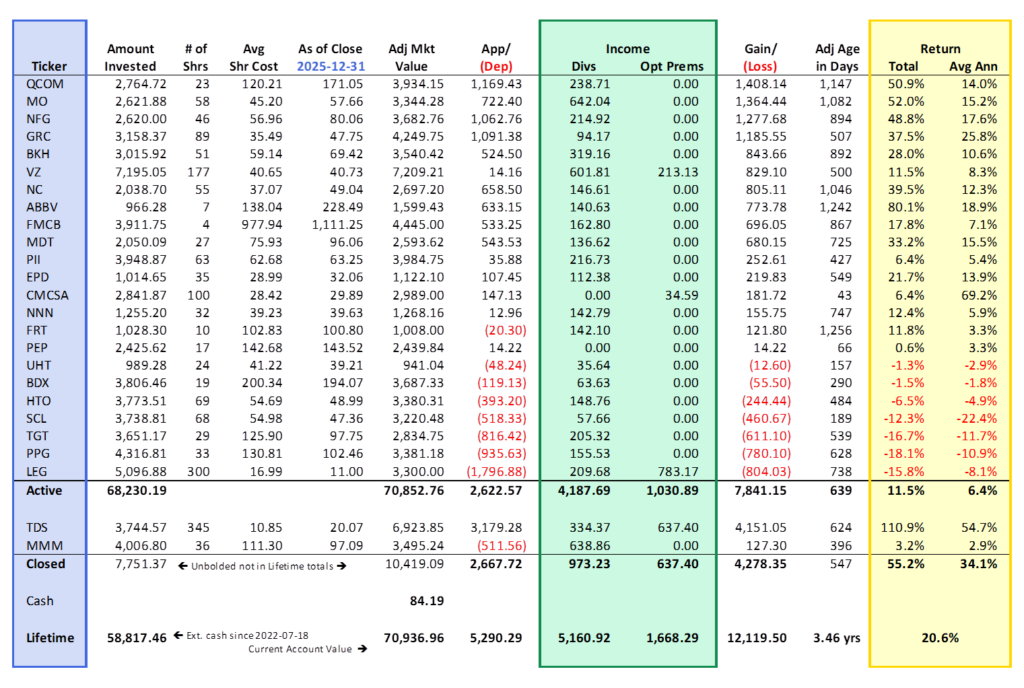

Below is the snapshot of the portfolio as of yesterday.

Observations

- Total return (includes realized and unrealized capital gains, dividends, and call premiums) is 20.6% since inception.

- Four stocks were added in 2025: CMCSA, PEP, SCL, and UHT.

- Active holdings have an annualized total return of 6.4%.

- 16 of the 23 current holdings are in positive territory.

Those are just the observations from the chart above. What is unseen is the importance of dividends. Only LEG has failed to increase its dividend. And even if it increases from here, their abdication of the throne (dividend reduction) in 2024 means the position will be closed as soon as it breaks even or better1. The other 22 stocks continue their long streaks of annual increases in their dividend.

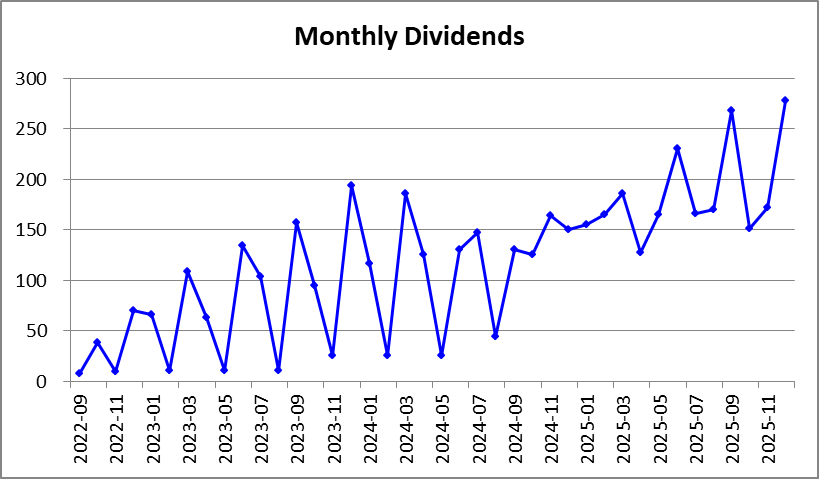

The figure in the chart above indicates that Royal Dividends has received $5,160.92 in dividends since inception. However, this figure includes $449.74 in proceeds from the SOLV spinoff from MMM in 2024Q2. Taking a closer look at the $4,711.14 in pure dividends on a monthly basis, we see quite a bit of volatility, largely because I’ve made no effort to select companies based on the months in which they pay dividends.

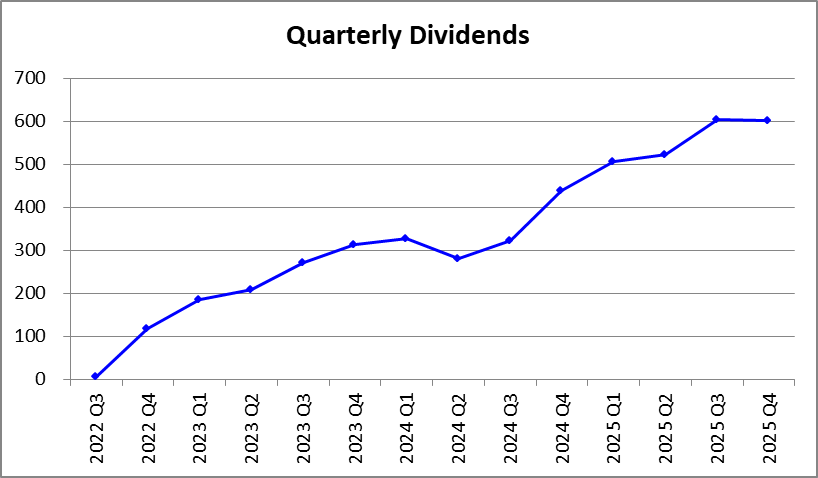

December 2025 was a record month. Of course, the picture smooths out on a quarterly basis.

Account value will ebb and flow with the whims of the market forces and the vicissitudes of business for individual stocks, but dividends should only ever grow. Portfolio dividends will grow through five forces:

- With the exception of LEG, each stock has a long history of increasing their dividend each year, with an average streak of 45 years.

- Dividends are reinvested.

- Any capital gains from the sale of a position are reinvested.

- Option premiums are reinvested.2

- Each week sees another $250+ of outside money invested.

The companies raise their dividends per share (#1), and we raise the number of shares (#2, #3, #4, and #5).

This is how wealth is amassed.

- Recently Somnigroup International Inc. made an unsolicited offer to acquire LEG for $12.00 a share. If LEG were to accept that offer in the next few months, it is unlikely we will be able to collect enough dividends and option premiums to offset the loss in the position before the acquisition is finalized. Will I be distraught if this should happen? Immeasurably so.

↩︎ - Positions with 100+ shares are eligible for covered call writing and this is the largest source of the $1,668.29 option premium collected to date. Currently, there are covered calls on CMCSA, LEG, and VZ. As the portfolio expands and additional holdings cross the 100‑share threshold, I expect option premiums to represent an increasingly meaningful share of total return. Even so, the fact that covered‑call writing added 1% to total return in 2025—with no capital appreciation forfeited through assignment—highlights how disciplined option writing can enhance performance without sacrificing upside. ↩︎