This week, seven of the portfolio holdings ranked in the Top 10.

| Ticker | Account Value |

| BDX | 3,530.77 |

| FMCB | 4,068.00 |

| HTO | 3,496.92 |

| PEP | 1,970.15 |

| PPG | 3,415.50 |

| SCL | 3,137.52 |

| VZ | 6,871.14 |

The lowest amount belongs to PEP. However, there exists a position imbalance such that only UHT is eligible for additional investment. Unfortunately, it is not ranked in the Top 10. That can only mean one thing.

It is time to add a new position to the Portfolio for the Ages!

Comcast Corp

Here is the profile from Schwab:

Comcast Corporation operates as a media and technology company worldwide. It operates through Residential Connectivity & Platforms, Business Services Connectivity, Media, Studios, and Theme Parks segments. The Residential Connectivity & Platforms segment provides residential broadband and wireless connectivity services, residential and business video services, sky-branded entertainment television networks, and advertising. The Business Services Connectivity segment offers connectivity services for small business locations, which include broadband, wireline voice, and wireless services; and ethernet network services for medium-sized customers and larger enterprises. The Media segment operates NBCUniversal’s national and regional cable networks; the NBC and Telemundo broadcast networks and owned local broadcast television stations; and Peacock, a direct-to-consumer streaming services. It also operates international television networks comprising the Sky Sports networks, as well as other digital properties. The Studios segment operates NBCUniversal and Sky film and television studio production and distribution operations. The Theme Parks segment operates Universal theme parks in Orlando, Florida; Hollywood, California; Osaka, Japan; and Beijing, China. The company also offers a consolidated streaming platforms under the Philadelphia Flyers and the Wells Fargo Center arena in Philadelphia, Pennsylvania; and Xumo. Comcast Corporation was founded in 1963 and is based in Philadelphia, Pennsylvania.

Obviously, the logo is excellent. It’s an extremely efficient way to portray a peacock.

And if you’ve ever watched TV, you’ve availed yourself of Comcast services.

The Details

Data as of 2025-10-24

| Name | Comcast Corp |

| Ticker | CMCSA |

| Website | Investor Relations |

| Sector | Communication Services |

| Dividend Streak | 17 years |

| Last Price | $29.28 |

| Div Amt (quarterly) | $0.33 |

| Ann Dividend | $1.32 |

| Last Ann Div Inc | 6.6% |

| Dividend Yield | 4.5% |

| Payout Ratio (ttm) | 28.5% |

| Beta (5-yr, mon) | 0.96 |

| P/E Ratio (ttm) | 6.62 |

Reasons to Invest

CMCSA is spinning off some of its cable channels: CNBC, E!, Golf Channel, MSNBC, Oxygen, SYFY, and USA. The resulting company will be publicly traded as Versant [VSNT] and shares will be given to existing shareholders. NBC and the Peacock streaming service will stay with CMCSA.

Now, as is customary in the months preceding an actual spin-off, the parent company will separate out the financials of the two entities so as to track the results going forward and recast previous financial statements so that reporting and historical comparisons make sense post spin-off. And in so doing we learn three things: (1) that Versant’s book of business has seen revenue decline over recent years, (2) that net income is also dropping, and (3) the reason for the spin-off is (1) and (2)

CMCSA essentially wants to shed the declining cable business from the more profitable internet and streaming services. That’s not to say shares of VSNT will be garbage; net income of $1.4 billion on $7 billion in revenue last year is nothing to sneeze at. But growing that business in the face of streaming competition is going to require real focus.

All that being said, the remainder of this brief post makes no attempt to assess CMCSA’s prospects as the company that it will be post spin-off, only as it is right now, which is impressive. And I’m not the only one who thinks so.

CFRA has a 12-month target of $40.00.

Morningstar has a fair value of $38.86.

Sure Dividend has a fair value of $41.00.

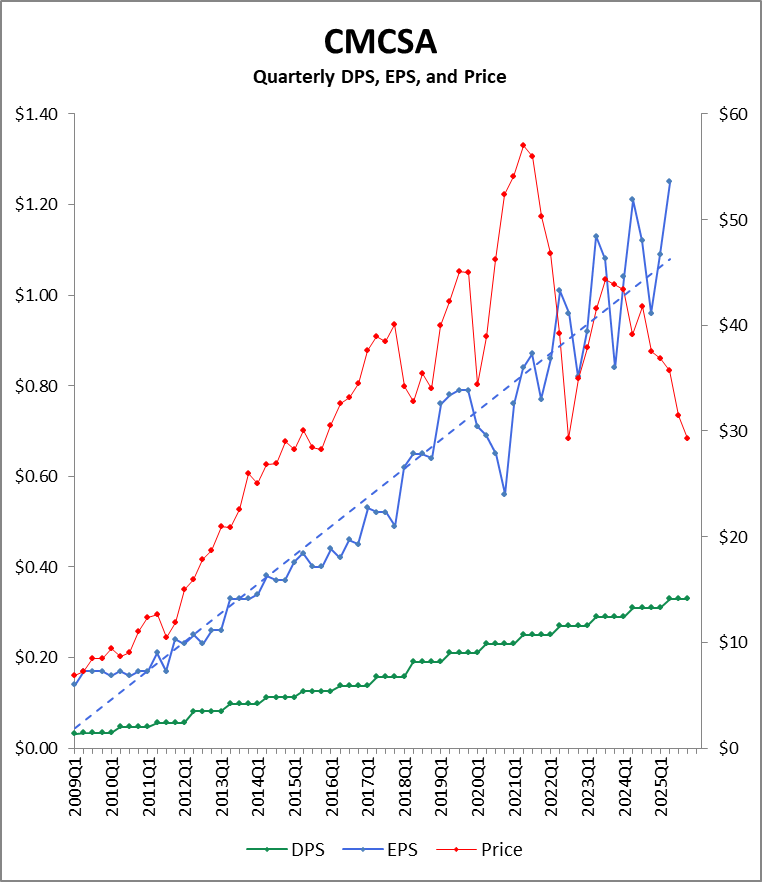

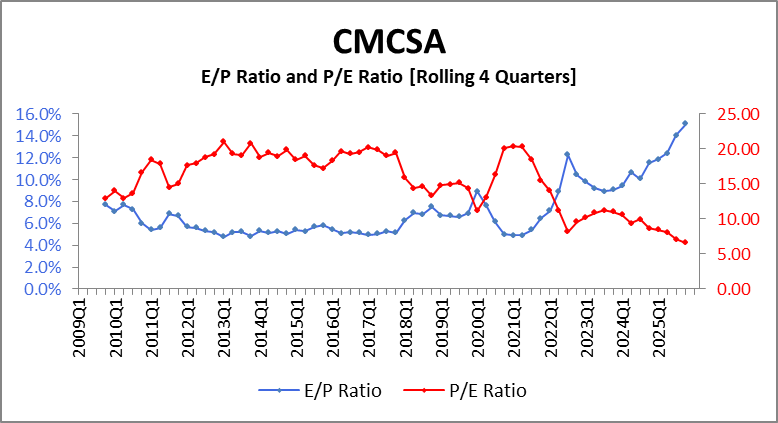

Yet, at $29.28 the market is only willing to pay $6.62 for each dollar of its earnings (P/E ratio). Insanity.

CMCSA first traded at $29.28 on 2014-12-30. But, 2025H1 EPS of $2.34 are 60% higher than CY2014 EPS of $1.46! Was $29.28 an absurd valuation at the end of 2014? Not unless you think a P/E ratio of 20 is absurd. There’s really nothing more I can say that the graph above doesn’t make abundantly clear.

In the best of times, CMCSA traded at P/E ratios just barely north of 20 – that level would be bankruptcy for Tesla Inc [TSLA]. Again, the market has assumed there is zero earnings growth left for CMCSA.

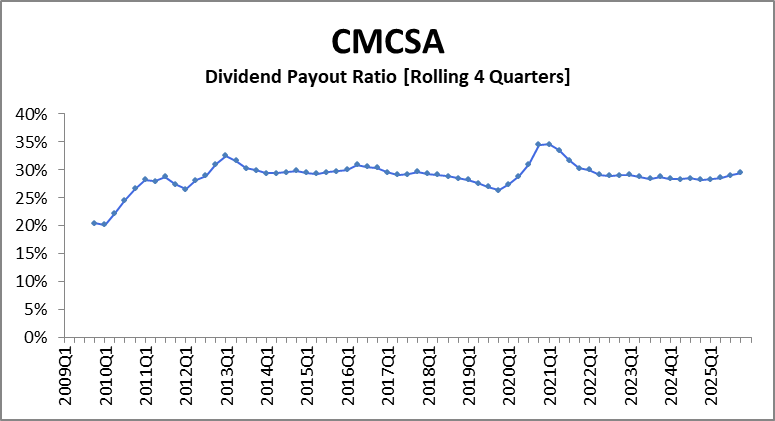

The dividend, which has increased for 17 consecutive years, is at an historically high yield and yet, no less safe than in any other year, with a payout ratio under 30%.

Quarterly earnings will be announced on 2025-10-30.

Will CMCSA continue its 4-year, 50% drop after the announcement? Will it even matter what the EPS are?

I want to have some stake in this game. I will be acquiring 34 shares of CMCSA on Monday morning.