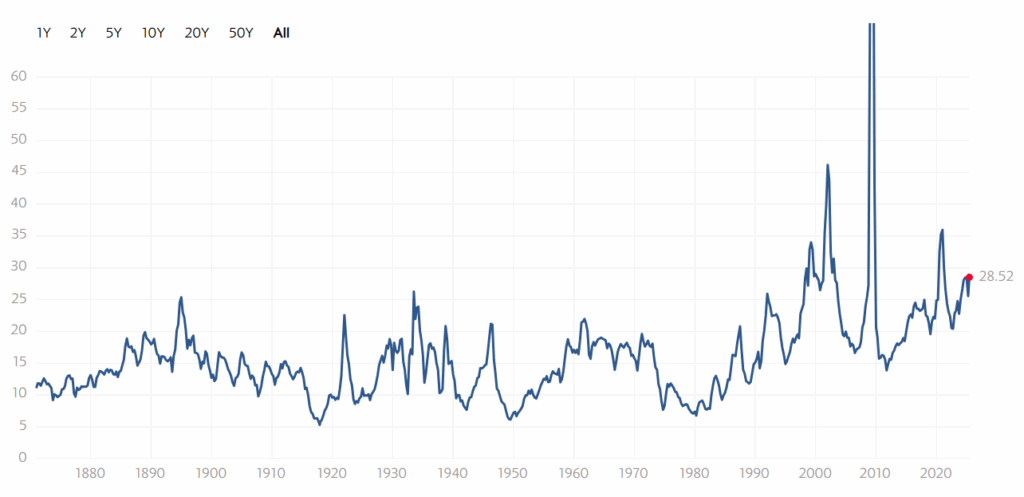

The S&P 500 Index [SPX] at 5,976.97 is just 170.46 points shy of its all-time high of 6,147.43 achieved on 2025-02-19. It feels inevitable that SPX will establish a new all-time high in short order. If it does achieve a new all-time high, how sustainable will that level be? Could it go even higher?

Let’s examine just one metric for both SPX and the Portfolio for the Ages: P/E ratio.

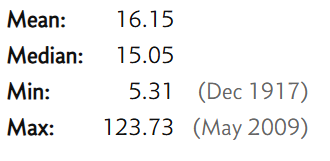

The S&P 500 [SPX] currently holds a P/E ratio of 28.52, placing it well above historical averages. As the data from Multpl suggests, this metric signals significant overvaluation.

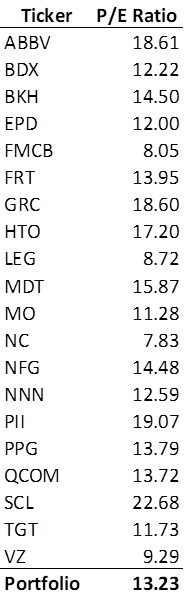

However, my focus isn’t on SPX. Royal Dividends owns 20 stocks, with only 9 belonging to the Index—what truly matters is the Portfolio for the Ages.

Notes:

- REITs (FRT & NNN) use Adjusted Funds from Operations (AFFO) instead of earnings.

- The portfolio’s average P/E ratio stands at 13.23, weighted by each stock’s allocation.

Observations

The table above tells a compelling story—while some valuations offer stocks the benefit of the doubt, others remain puzzlingly low.

- PII recently posted its worst quarterly earnings in recent history (negative), yet its P/E ratio exceeds the SPX mean.

- SCL has endured weak earnings lately, yet its price suggests confidence in a rebound.

- LEG struggles under heavy debt as elevated interest rates and recessionary pressures weigh on consumer discretionary spending.

- NC, true to form, trades at a laughably low valuation, but this is consistent with its typical P/E behavior. Being small, cyclical, and coal-focused, NC remains perpetually discounted.

- FMCB & VZ trade at shockingly low levels—not just relative to SPX, but compared to their own historical valuations.

Outlook

While performance has been sluggish, a portfolio P/E of 13.23 suggests ample upside. A return to SPX’s historical mean alone would imply a 22% gain.

That said, unlike the overvalued SPX, the Portfolio for the Ages is meaningfully undervalued. However, I don’t anticipate a sharp rally in these stocks in the near term. The more likely scenario? SPX corrects downward, particularly through sector rotation:

Overinflated tech stocks—including the Magnificent 7—shed some excess valuation.

Undervalued companies hold firm, then gradually reclaim ground—not just relative to SPX, but in absolute terms as well.

At least that’s what we hope for.