This week is the third and final ‘off’ week intended to restore the $250+ per week pace of investment which became necessary with the establishment of a position in BDX. Read on to find out which position would have been most worthy of new money.

This week, four of the portfolio holdings ranked in the Top Ten: BDX, PII, PPG, and SJW.

| Ticker | Account Value |

| BDX | 1,370.94 |

| PII | 1,091.17 |

| PPG | 3,370.64 |

| SJW | 3,110.94 |

The lowest amount belongs to PII. There is nothing precluding further investment in that position, other than it being an ‘off’ week.

At this time, Royal Dividends has three active orders:

- GTC Limit Order to Buy 1 Share of FMCB for $975 or Less

- GTC Limit Order to Sell to Open 3 2025-03-21 $12.50 Calls on LEG for $0.40 or More per Share

- GTC Limit Order to Sell to Open 1 2025-04-17 $45.00 Calls on VZ for $0.40 or More per Share

I will continue to let these orders work.

Market Commentary

The equally weighted S&P 500 has dropped on 14 of the 18 trading days so far in December. Friday was another blow, and December sits at a 6% loss so far. The active holdings of the Portfolio of the Ages were once north of 17% annualized and now sits at about 1%. Below are the five positions with unrealized losses, the bottom two of which have had extraordinarily poor performance.

The performance of these companies, particularly LEG and PII saddens me. Their earnings while still positive, are down, and so some price decline is to be expected. Tax loss harvesting is also suspect here as the price declines in December have been entirely unjustified by any company specific or broader market news. I expect PII to turnaround quicker then LEG when the cyclical nature of their respective businesses comes around again; PII has the stronger balance sheet. As to when that happens, no one knows.

We may yet have a rather brutal recession as would typically be the case after such a long period of yield curve inversion. If so, further draw-down is possible.

Note how the recessions (in shaded gray columns) materialize after each yield curve inversion ends. Might we be looking at some darker (grayer) days ahead? Count on it. My questions: is the market anticipating a recession, and if so, how much has been baked into the prices of the portfolio stocks already?

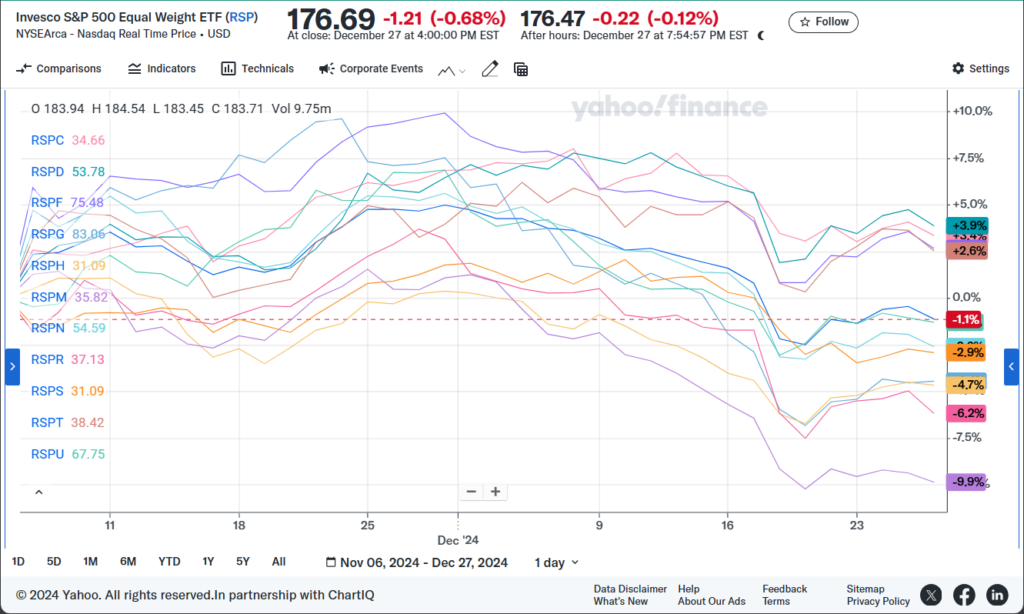

The equally weighted S&P 500, up 13.1% through election day, has returned -1.1% since election day. This relatively flat performance masks significant sector rotation underneath the surface.

The red rectangle showing -1.1% represents the whole, equally weighted index [RSP]. Consumer Discretionary [RSPD] has performed the best at +3.9%. Materials [RSPM] has performed the worst at -9.9%, and Real Estate [RSPR] second most atrocious at -6.2%. Of course, Technology [RSPT] is near the top at +2.6% and I suspect it is a matter of time before it is the only one still above water.

The performance of RSPD only adds further insult to the performance of two of its members, LEG and PII.

If I feel at all inspired in the coming days, I will report further on portfolio performance as another year disappears into the sludge.